SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

MANILA, Philippines – “Credit cards? Demonyo yun (Credit cards? They are the devil.)” said one commenter on Rappler’s post asking people about credit applications.

According to the World Bank’s 2017 Global Findex Database, only 1.9% of Filipinos aged 15 and up own a credit card. The same index also says only 4.4% borrow money from formal financial institutions.

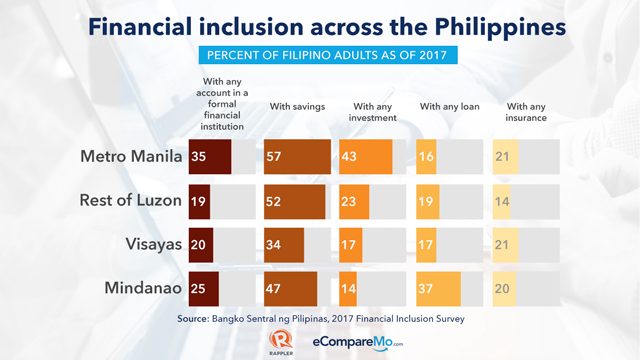

In a survey conducted by the Bangko Sentral ng Pilipinas on financial inclusion (meaning access to financial products and services), the leading cause for Filipinos to not have formal financial accounts—whether it’s a bank account, a credit card, or a loan—is a perceived “lack of need” (21%). However, this belief in not needing financial products is refuted by the World Bank’s data as their study shows that, in practice, close to three-fourths of Filipinos (72.3%) still borrow cash from informal sources.

While we can’t discount that financial inclusion is worst among the poor based on BSP data, this finding also showcases a disconnect between perception and reality. And though people may think they do not need financial services such as loans and credit cards, the majority actually do but end up resorting to riskier means just to get the extra cash they need.

Add to this the other reasons the BSP discovered why Filipinos don’t have accounts—their inability to provide documentary requirements (18%), not knowing the process (9%)— we get to understand that the first barrier for many when it comes to financial inclusion: the people themselves.

No application, no rejection…no problem?

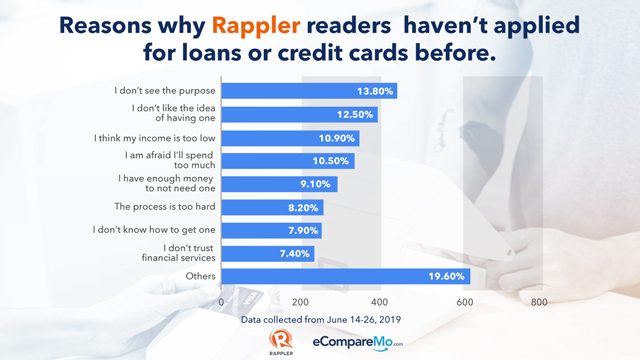

From June 16 to June 28 of this year, a separate survey was conducted on the Rappler and eCompareMo websites to gauge audience sentiment on financial instruments such as loans and credit cards.

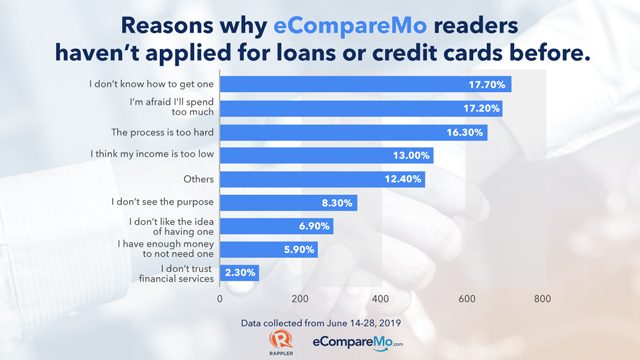

Consistent with BSP and World Bank’s findings, Rappler respondents also said that they don’t see the need or don’t like the idea of having a credit card or an outstanding loan. eCompareMo respondents, on the other hand, are held back by their lack of knowledge in the application process.

Further answers revealed that, in a nutshell, whatever life stage a person may be in, they will have their own reasons for not getting a credit card or a loan.

Yuppies in their early 20’s would rather use cash as they have this fear that they will spend too much when given the extra “purchasing power” of a credit card. While those “adulting” in their late 20’s to 30’s feel that they are already taking on responsibilities which they have to prioritize given their limited income.

The sad part is that, based on the survey, when respondents start seeing the value of credit cards and loans, they are already in their 40’s and 50’s, and they already find the process too hard to follow.

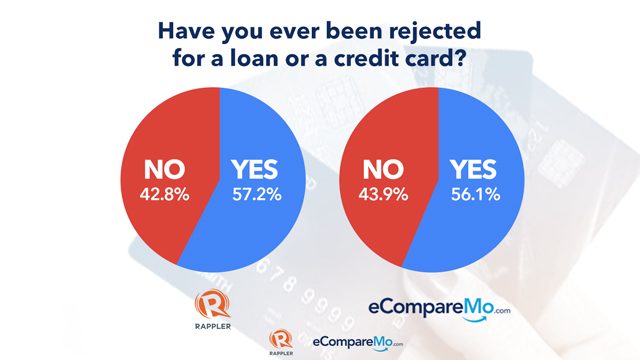

And from this same segment, those that were able to apply, the majority of them have been rejected once or twice.

Most of them think it’s because they have a low income or have no credit history. The rest don’t have an idea why. These respondents say that the rejection discouraged them from applying for credit in the foreseeable future.

They would rather opt to avail of less secure and more expensive options such as via loan sharks, payday loan, or other informal alternatives.

Understanding the process

Again, the first barrier is oneself. To truly make the most out of credit cards and other financial services, you have to be responsible and make an effort to understand the products you are availing, as well as the terms and agreements that come with them. This is the best way to ease apprehensions and debunk misconceptions.

For one, shake off the idea that credit cards and other financial products are forms of debt. Credit cards can be multi-faceted and come with different features, benefits, and exclusive offers. Thus, unlike debt, you can gain more than what you spend when you use your credit card right.

Secondly, credit cards can be more organized and more convenient than cash. For those wanting to take control of their finances, credit card transactions are more manageable to track. They can also be safer to bring than money at times, as you can have a card blocked when you lose it.

When you do start applying for credit, knowing the process helps counter the widespread fear of rejection. What you can do first is to learn about your credit score.

You have to understand that when you apply for a credit or a loan, your application will go through an “underwriting process.” An “underwriter” is someone who will assess how risky you can be in terms of repayment. This includes looking at your credit score.

Knowing your credit score

Credit scores are 3-digit numbers that represent your ability to pay based on your previous transactions, your credit history. You can check your credit score by getting a free copy of your credit report from your bank, the Credit Information Corporation (CIC), or one of the CIC’s accredited bureaus.

(This will also help you see if there are any outstanding loans or unpaid debts, you’re unaware of.)

And contrary to popular belief, income and assets don’t affect your credit score. Nor does age, gender, and other non-credit related banking information such as existing savings and checking accounts.

A good credit score will not only increase your chances of credit card or loan approval, but it will also help you get higher loan amounts and lower interest rates. It can also benefit your other applications in insurances and property rentals. Some employers even look at credit score when they do background checks.

If you fear that you don’t have a credit history (how can you get credit history if you can’t even get a card, right?), then you may need to check the card you’re applying for. As mentioned earlier, cards are not “one size fits all.” There are prepaid cards, and there are also starter cards that require minimal requirements and have simple application procedures that you can avail.

You can build your credit score from there.

Embracing financial freedom

Application is just the first step. Maintenance is the tricky part.

Keep your credit score healthy by paying your dues on time. Also, do it consistently. These all reflect on your credit history.

Furthermore, don’t be afraid to reach out to your banks. Contrary to popular belief, terms are negotiable. You can even request for annual fees to be waived and for lower interest rates.

There are also various tools now that can empower you to take control of your finances better. eCompareMo, for instance, provides customers with online comparison tools that help them find credit card and loan products they’ll most likely get approved for.

The site also matches consumers with car, travel, and health insurance providers tailor-fit for their budget and needs.

This article is just the first part of our #RejectED series on credit education. Stay tuned for our live roundtable with policymakers and finance experts on July 30, Tuesday, 11 am. – Rappler.com

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.