SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[Ask the Tax Whiz] Is a donation an allowable deduction?](https://www.rappler.com/tachyon/2021/08/shutterstock-donation-ls.jpg)

Except for employees or those earning compensation income, individual and corporate taxpayers have allowable deductions from gross income. These include but are not limited to ordinary and necessary business expenses as provided under Section 34 of the tax code.

Charitable and other contributions or donations may also be claimed as deductible expenses in full or subject to limitations.

If I make a donation to the government, is it deductible in full?

Yes, provided the donation to the government will be exclusively used to undertake priority activities in education, health, youth and sports development, human settlements, science and culture, and economic development, according to the National Priority Plan determined by the National Economic and Development Authority. Otherwise, it will be subject to limitations as prescribed in Section 34(H)(1).

When is a donation to a charitable organization deductible in full? If not, how much can I claim as a deductible expense?

Donations to accredited non-governmental organizations are deductible in full. As provided under Section 34(H)(2)(c), an NGO refers to a non-profit domestic corporation:

1. Organized and operated exclusively for scientific, research, educational, character-building and youth and sports development, health, social welfare, cultural or charitable purposes, or a combination thereof, no part of the net income of which benefits any private individual;

2. Which, not later than the 15th day of the third month after the close of the accredited NGO’s taxable year in which contributions are received, uses the donation for activities constituting the purpose for which it is operated, unless an extended period is granted by the secretary of finance, upon recommendation of the commissioner;

3. The level of administrative expense of which shall, on an annual basis, conform with the rules and regulations to be prescribed by the secretary of finance, upon recommendation of the commissioner, but in no case to exceed 30% of the total expenses; and

4. The assets of which, in the event of dissolution, would be distributed to another non-profit domestic corporation organized for a similar purpose, or to the state for public purpose, or would be distributed by a court to another organization to be used for the purpose for which the dissolved organization was organized.

Donations made to entities other than the government and accredited NGOs as provided under Section 34(H)(2) are subject to limitations. Allowable deductions must not exceed the limit based on taxable income before claiming donations:

- For individuals – not in excess of 10%

- For corporations – not in excess of 5%

Whether I claim my donations in full or not as deductible expense, will I be subject to donor’s tax? How much do I need to pay to claim it as an allowable deduction?

Under the Tax Reform for Acceleration and Inclusion (TRAIN) law, if your donations do not exceed P250,000 per year, you are exempted from donor’s tax regardless of the recipient or donee status. Moreover, under Section 101(A), the following gifts or donations shall be exempt from donor’s tax:

1. Gifts made to or for the use of the national government or any entity created by any of its agencies which is not conducted for profit, or to any political subdivision of the government; and

2. Gifts in favor of an educational, charitable, religious, cultural or social welfare corporation, institution, accredited NGO, trust or philanthropic organization, or research institution or organization, provided that not more than 30% of the gifts shall be used by such donee for administration purposes. The recipient is defined as a non-stock entity, paying no dividends, governed by trustees who receive no compensation, and devoting all its income, whether students’ fees or gifts, donation, subsidies, or other forms of philanthropy, to the accomplishment and promotion of the purposes enumerated in its articles of incorporation.

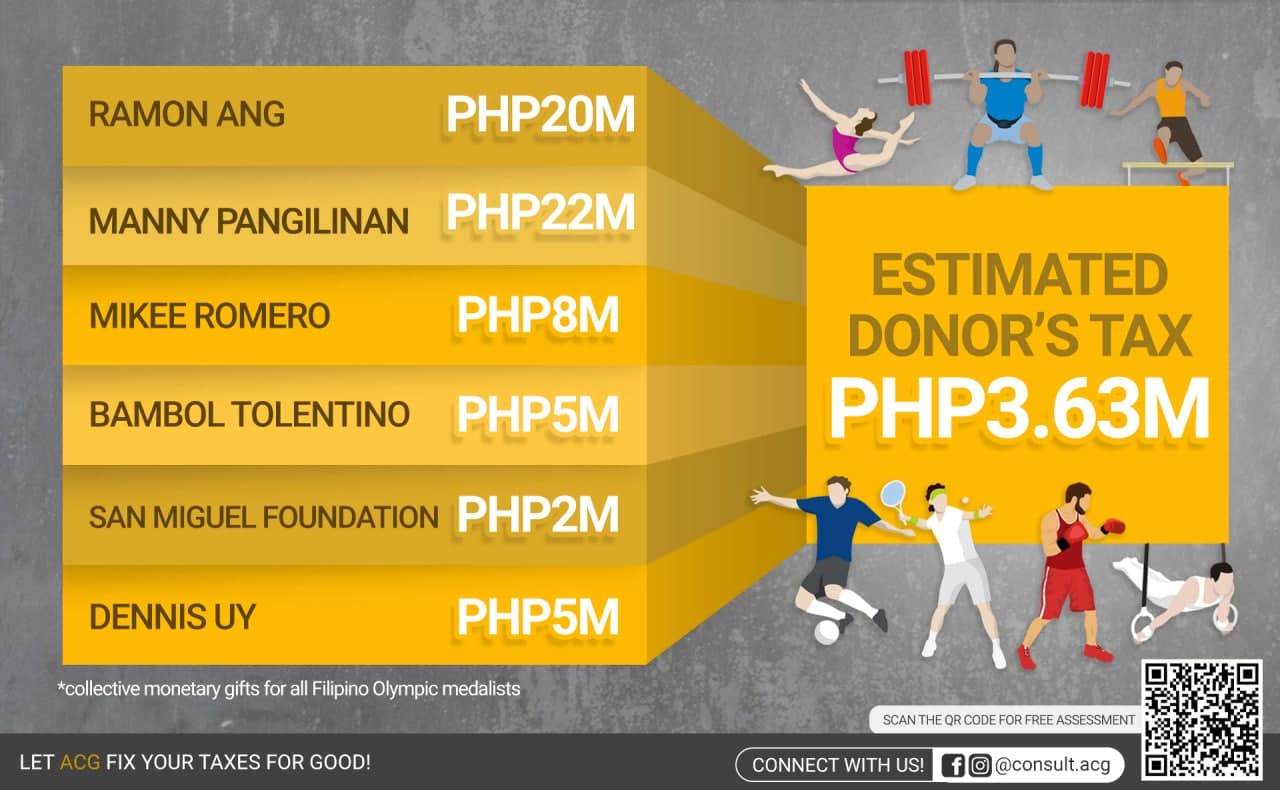

If a gift or donation exceeds P250,000 or it is not included in the exception under Section 101(A), it shall be subject to fixed 6% donor’s tax as amended under the TRAIN law effective January 1, 2018. Donors must pay the donor’s tax within 30 days after the date the gift is made. In the case of the cash and non-cash gifts given to Olympic gold medalist Hidilyn Diaz and other athletes, donors must pay the donor’s tax before they can claim it as a deductible expense.

Know your taxes to stay out of trouble with the Bureau of Internal Revenue. Want to save money from taxes and keep your business worry-free? For more tax updates and information, follow the Asian Consulting Group on Facebook or email us at consult@acg.ph for a free tax assessment. You may also use the QR code in the image above. – Rappler.com

Mon Abrea, CPA, MBA, is the co-chair of the Paying Taxes-EODB Task Force. With the TaxWhizPH mobile app as his brainchild, he was recognized as one of the Outstanding Young Persons of the World, an Asia CEO Young Leader, and one of the Ten Outstanding Young Men of the Philippines because of his tax advocacy and expertise. Currently, he is the chairman and CEO of the Asian Consulting Group and trustee of the Center for Strategic Reforms of the Philippines – the advocacy partner of the Bureau of Internal Revenue, Department of Trade and Industry, and Anti-Red Tape Authority on ease of doing business and tax reform. Visit www.acg.ph for more information or email him at mon@acg.ph and download the TaxWhizPH app for free if you have tax questions.

Add a comment

How does this make you feel?

![[Ask The Tax Whiz] How to file annual income tax returns for 2023](https://www.rappler.com/tachyon/2022/11/tax-papers-hand-shutterstock.jpg?resize=257%2C257&crop_strategy=attention)

There are no comments yet. Add your comment to start the conversation.