SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

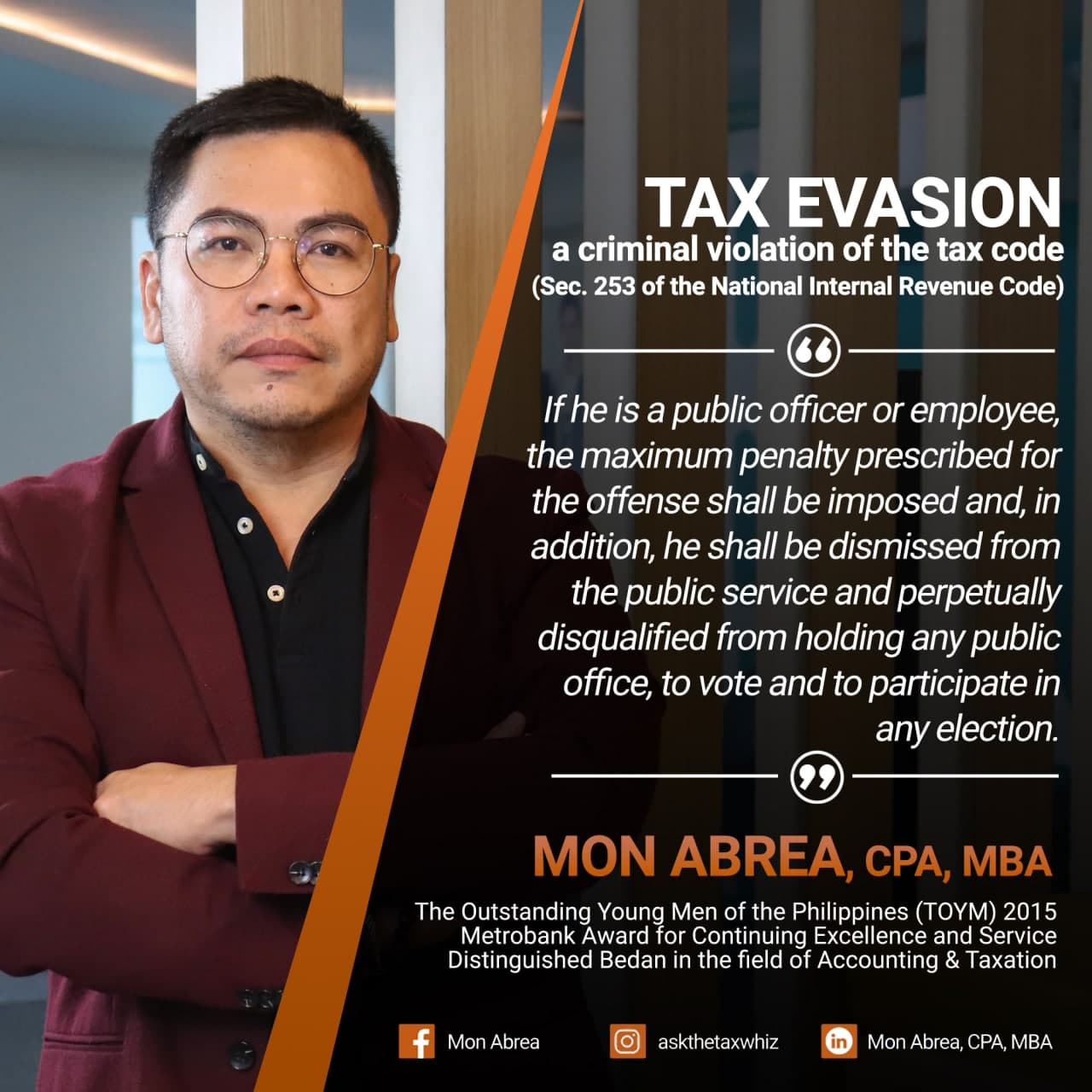

![[Ask the Tax Whiz] Tax evasion: Liabilities of candidates, foreigners, accountants](https://www.rappler.com/tachyon/2022/07/tax-evasion-20170620_1.jpg)

Run After Tax Evaders (RATE) is one of the enforcement programs of the Bureau of Internal Revenue (BIR). Are political candidates and government officials exempted from being charged with tax evasion? What will happen if they’re found guilty? What constitutes prima facie evidence of tax fraud, or of violations of the tax code? When does the tax investigation begin?

Political candidates and government officials may be charged with tax evasion once prima facie evidence of tax fraud has been established by the BIR. Section 253(c) of the tax code provides that “if the offender is a public officer or employee, the maximum penalty prescribed for the offense shall be imposed and, in addition, he shall be dismissed from the public service and perpetually disqualified from holding any public office, to vote and to participate in any election.”

Prima facie evidence of tax fraud is provided in Section 248(B): “in case of willful neglect to file the return within the period prescribed by this Code or by rules and regulations, or in case a false or fraudulent return is willfully made, the penalty to be imposed shall be fifty percent (50%) of the tax or of the deficiency tax, in case, any payment has been made on the basis of such return before the discovery of the falsity or fraud: Provided, that a substantial under-declaration of taxable sales, receipts or income, or a substantial overstatement of deductions, as determined by the Commissioner pursuant to the rules and regulations to be promulgated by the Secretary of Finance, shall constitute prima facie evidence of a false or fraudulent return.”

The formal investigation of a RATE case, including examination of the taxpayer’s book of accounts, accounting records, and third-party records, through the issuance of a letter of authority and/or access letters (if warranted), will begin only after prima facie evidence of fraud or tax evasion has been established.

Is payment of penalties a valid defense in prosecution for violation of the tax code? Is filing false or fraudulent tax returns subject to penalties of perjury?

No, it is not a valid defense. Pursuant to Section 253(a) of the tax code, “any person convicted of a crime penalized by this Code shall, in addition to being liable for the payment of the tax, be subject to the penalties imposed herein: Provided, that payment of the tax due after apprehension shall not constitute a valid defense in any prosecution for violation of any provision of this Code or in any action for the forfeiture of untaxed articles.”

Yes, filing fraudulent tax returns is considered perjury. Section 267 of the tax code provides that “any person who willfully files a declaration, return or statement containing information which is not true and correct as to every material matter shall, upon conviction, be subject to the penalties prescribed for perjury under the Revised Penal Code.”

Are foreigners doing business in the Philippines liable to pay taxes? Can they do business without BIR registration? If charged with tax evasion, would they be deported? How about those who assisted them in evading taxes?

Every person or entity subject to any internal revenue tax is required to register with the appropriate revenue district office of the BIR before starting a business.

Failure to register with the BIR is one of the criminal tax violations covered by the RATE program.

Foreigners who commit tax evasion will be deported. Section 253(c) of the tax code provides that “if the offender is not a citizen of the Philippines, he shall be deported immediately after serving the sentence without further proceedings for deportation.”

Further, Section 253(b) of the tax code provides that “any person who willfully aids or abets in the commission of a crime penalized herein or who causes the commission of any such offense by another shall be liable in the same manner as the principal.”

Can a financial officer or independent certified public accountant be held liable for reporting or signing financial statements with material misstatement/s? Can his or her CPA license be revoked for tax evasion? How about the management or officers and other employees who are also involved in the attempt to evade taxes?

Financial officers and CPAs have penal liability for making false entries, records, or reports as provided in Section 257(a) of the tax code, which covers “any financial officer or independent Certified Public Accountant engaged to examine and audit books of accounts of taxpayers under Section 232 (A) and any person under his direction who:

(1) Willfully falsifies any report or statement bearing on any examination or audit, or renders a report, including exhibits, statements, schedules or other forms of accountancy work which has not been verified by him personally or under his supervision or by a member of his firm or by a member of his staff in accordance with sound auditing practices; or

(2) Certifies financial statements of a business enterprise containing an essential misstatement of facts or omission in respect of the transactions, taxable income, deduction and exemption of his client shall be subjected to penal liabilities. In case the person is not an independent CPA or financial officer as long as he makes false entries, records or reports, or using falsified or fake accountable forms he shall be also subjected to said penalties.”

Upon conviction, his or her CPA license shall be revoked automatically as provided in Section 253(c) of the tax code: “If the offender is a Certified Public Accountant, his certificate as a Certified Public Accountant shall, upon conviction, be automatically revoked or cancelled.”

Moreover, officers and other employees who are also involved in violating the tax code as provided in Section 253(d) would be penalized: “In the case of associations, partnerships or corporations, the penalty shall be imposed on the partner, president, general manager, branch manager, treasurer, officer-in-charge, and the employees responsible for the violation.”

Don’t wait for the BIR to run after you or your company for failure to comply with the tax code. Get an Annual Tax Health Check now by emailing us at consult@acg.ph or call (+63)9063159230. Join the Executive Tax Management Program of the Asian Consulting Group to manage your taxes without stress and unnecessary penalties, interest, and compromises. Register now through this link or visit www.acg.ph for more information.

– Rappler.com

Mon Abrea, CPA, MBA, is the co-chair of the Paying Taxes-EODB Task Force. With the TaxWhizPH mobile app as his brainchild, he was recognized as one of the Outstanding Young Persons of the World, an Asia CEO Young Leader, and one of the Ten Outstanding Young Men of the Philippines because of his tax advocacy and expertise. Currently, he is the chairman and CEO of the Asian Consulting Group and trustee of the Center for Strategic Reforms of the Philippines – the advocacy partner of the Bureau of Internal Revenue, Department of Trade and Industry, and Anti-Red Tape Authority on ease of doing business and tax reform. Visit www.acg.ph for more information or email him at mon@acg.ph and download the TaxWhizPH app for free if you have tax questions.

Add a comment

How does this make you feel?

![[Ask The Tax Whiz] How to file annual income tax returns for 2023](https://www.rappler.com/tachyon/2022/11/tax-papers-hand-shutterstock.jpg?resize=257%2C257&crop_strategy=attention)

![[Ask The Tax Whiz] Are cross-border services taxed in the Philippines?](https://www.rappler.com/tachyon/2024/02/bpo-workers.png?resize=257%2C257&crop=72px%2C0px%2C785px%2C785px)

![[Ask the Tax Whiz] Ease of paying taxes law: What you need to know](https://www.rappler.com/tachyon/2023/02/calculate-february-22-2023.jpg?resize=257%2C257&crop_strategy=attention)

There are no comments yet. Add your comment to start the conversation.