How Filipinos are coping with inflation

Consumers and business owners alike feel the pain of rising prices.

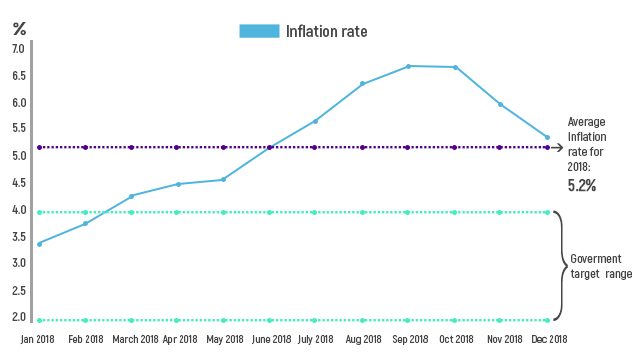

Prices of goods and services made a sudden jump in 2018.

While the uptick started to ease in November , the average figure for the year was still beyond the government’s limit.

Filipino consumers feel a tight squeeze on their pockets.

A survey conducted by data insights company TheNerve shows 46% of respondents feeling financially worse off in 2018 because of higher prices and household expenses.

With 46% seeing no increase in their paychecks, most say they’re buying only the basics (42%), and would rather save than make any big purchase (25%).

They don’t have plans or have postponed plans to buy a house or a car or even durable goods like laptops, cellphones, and home appliances. Food and other basic needs are the top priority, they contend.

Small business owners sing the same tune. They say their production volume and income either stayed the same or were down from 2017, while their costs remained at the same level or went up.

They cite rising prices of goods as the number one factor limiting their ability to expand.

Taking out bank loans could potentially help, but that’s not an option for them right now.

The main reason: higher interest rates.

Prices of goods and services made a sudden jump in 2018.

While the uptick started to ease in November, the average figure for the year was still beyond the government’s limit.

Filipino consumers feel a tight squeeze on their pockets.

A survey conducted by TheNerve shows 46% of respondents feeling financially worse off in 2018 because of higher prices and household expenses.

With 46% seeing no increase in their paychecks, most say they’re buying only the basics (42%), and would rather save than make any big purchase (25%).

They don’t have plans or have postponed plans to buy a house or a car or even durable goods like laptops, cellphones, and home appliances. Food and other basic needs are the top priority, they contend.

Small business owners sing the same tune. They say their production volume and income either stayed the same or were down from 2017, while their costs remained at the same level or went up.

They cite rising prices of goods as the number one factor limiting their ability to expand.

Taking out bank loans could potentially help, but that’s not an option for them right now.

The main reason: higher interest rates.

The Bangko Sentral ng Pilipinas (BSP) aggressively raised its benchmark interest rates last year.

In case you’re not familiar with the central bank’s role, its mandate is to maintain stable prices to promote sustainable economic growth and preserve the value of money.

To do that, it must calibrate interest rates to a level that’s helpful for the economy.

If the economy needs to grow, the central bank supplies more credit to banks for lending. It also lowers the interest rates it charges banks when they borrow from it, in turn making it cheaper for banks to lend to their clients.

When banks lend more to businesses at attractive rates, those businesses are able to buy more raw materials and expand, employ more people, and boost people’s pay. The same goes for consumers: with the abundance of cheap loans, they’re able to afford more stuff they need and want.

That kind of spending stirs the economy. However, the strong demand for goods also tends to drive their prices up.

We have to avoid prices going up too fast to the point where people don’t want to spend. Businesses would see slower sales and may slash jobs. People will lose their incomes and the whole situation goes on a downward spiral.

So for the BSP it’s a balancing act. If it wants to put some brakes on the economy and prevent inflation from escalating to potentially dangerous levels, it lessens the supply of credit. In the chart you’ll see you how the BSP’s key policy rate (reverse repurchase rate) rises when inflation picks up.

The BSP also raises the interest rates it charges banks, which banks pass on to their clients.

Higher interest rates discourage people from borrowing money and spending. House and car loans and even credit card payments become expensive.

People who already have loans will have to pay banks more, so that eats into their disposable income and causes them to cut back on spending.

Small businesses with limited cash flow get affected, too. They may find it difficult to afford loans, so they put off expansion plans.

Those who have loans with fluctuating interest rates may find them hard to repay. Worst-case scenario, with mounting costs, they may not earn any profit and be forced to cut jobs.

So for the BSP it’s a balancing act. If it wants to put some brakes on the economy and prevent inflation from escalating to potentially dangerous levels, it lessens the supply of credit.

The BSP also raises the interest rates it charges banks, which banks pass on to their clients.

Higher interest rates discourage people from borrowing money and spending. House and car loans and even credit card payments become expensive.

People who already have loans will have to pay banks more, so that eats into their disposable income and causes them to cut back on spending.

Small businesses with limited cash flow get affected, too. They may find it difficult to afford loans, so they put off expansion plans.

Those who have loans with fluctuating interest rates may find them hard to repay. Worst-case scenario, with mounting costs, they may not earn any profit and be forced to cut jobs.

Going back to how the BSP calibrates rates, some camps have argued that runaway inflation in 2018 was not caused by strong demand for goods but supply-related issues.

Those issues included the uptick in prices of world oil and other imports - both affected by the peso’s weakness, and shortage in supply of some agricultural products like rice. Adding fuel to the fire was the TRAIN law which implemented new excise taxes on certain products like oil.

That has prompted them to question the BSP’s move to crank up interest rates which could hurt the growth of the economy (remember that consumer spending is a key growth driver).

But the BSP says it raised rates to defend the peso - higher rates attract foreigners to invest in Philippine securities, increasing the demand for the local currency and its value.

The central bank adds that the move was supposed to rein in inflation expectations - a factor that could worsen inflation itself.

If people and businesses expect future inflation to go up, it could become a self-fulfilling prophecy.

That’s because workers are more likely to ask for pay increments, which would give them more disposable income. And firms expecting higher costs from rising prices and potential wage increases will incorporate those factors in their pricing.

Another thing about inflation expectations: people tend to purchase more goods today if they think prices will pick up further in the future.

All those things feed into actual prices.

Both consumers (56%) and business owners (53%) in our surveys expect inflation to speed up more in the coming months.

Business owners say they will cope by looking for cheap inputs, trimming costs such as labor, or increasing their selling price.

However, even with elevated inflation expectations, consumers aren’t inclined to buy goods before they get more expensive. They’re tightening their belts instead.

Indeed, hiked inflation and interest rates have already affected consumer spending, slowing the country’s economic growth in the third quarter of 2018.

However, as of November and December, the inflation rate has abated , thanks to easing world oil prices, government measures to improve agricultural supply, and a better peso. The BSP also hit the pause button on rate hikes during its December meeting.

The central bank expects inflation to return within the target in 2019, and promises to keep a close watch on any developments that could negatively affect it.

While consumers think inflation will still increase, they’re hopeful it will be offset by pay gains.

Both consumers (56%) and business owners (53%) in our surveys expect inflation to speed up more in the coming months.

Business owners say they will cope by looking for cheap inputs, trimming costs such as labor, or increasing their selling price.

However, even with elevated inflation expectations, consumers aren’t inclined to buy goods before they get more expensive. Instead, they’re tightening their belts.

Indeed, hiked inflation and interest rates have already affected consumer spending, slowing the country’s economic growth in the third quarter of 2018.

However, as of November and December, the inflation rate has abated , thanks to easing world oil prices, government measures to improve agricultural supply, and a better peso. The BSP also hit the pause button on rate hikes during its December meeting.

The central bank expects inflation to return within the target in 2019, and promises to keep a close watch on any developments that could negatively affect it.

While consumers think inflation will still increase, they’re hopeful it will be offset by pay gains.

Inflation is a fixture in the economy. It’s here to stay. The best way to combat it is to prepare for it.

One of the things consumers can do to inflation-proof their life is invest. Invest in assets that grow in value over time, such as stocks or real estate. And invest in yourself. Always strive to learn new and in-demand skills. Nothing is more powerful than boosting your earning power.

For businesses, it’s advisable to raise selling prices in small amounts rather than one big jump. Some of your competitors would probably do the latter; that gives you an edge to win more customers.

Make sure you have cash reserves to help you with surging costs. With the onslaught of inflation, costs often rise faster than you can increase your selling price.

You can also try to renegotiate contracts with suppliers who may be willing to give you discounts for pre or bulk orders.

Finally, mind your margins and focus on earning profits from the get-go, not just during tough times.

Sources:

- Inflation rates from the Philippine Statistics Authority

- Reverse repurchase rates from BSP

- Overnight lending rates from BSP

- Average bank lending rates from BSP