SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[ANALYSIS] Why is the PH stock market among world’s worst?](https://www.rappler.com/tachyon/r3-assets/1D8282F5338E42229474649A5D9CE011/img/811E279B41F843A393523B3BEBBFF35A/Why-is-the-Philippine-stock-market-now-among-the-worlds-worst-October-24-2018.jpg)

It’s been a tough year for the Philippine economy thus far. Not only is the Philippine peso one of the weakest currencies in ASEAN, but Philippine inflation is also the highest.

There is a third way our economy stands out in the region this year: as of last week, the Philippine Stock Exchange Index (PSEI) fell by 18% since the beginning of 2018, becoming the worst-performing stock market in ASEAN.

In early October, it actually fared as the world’s worst.

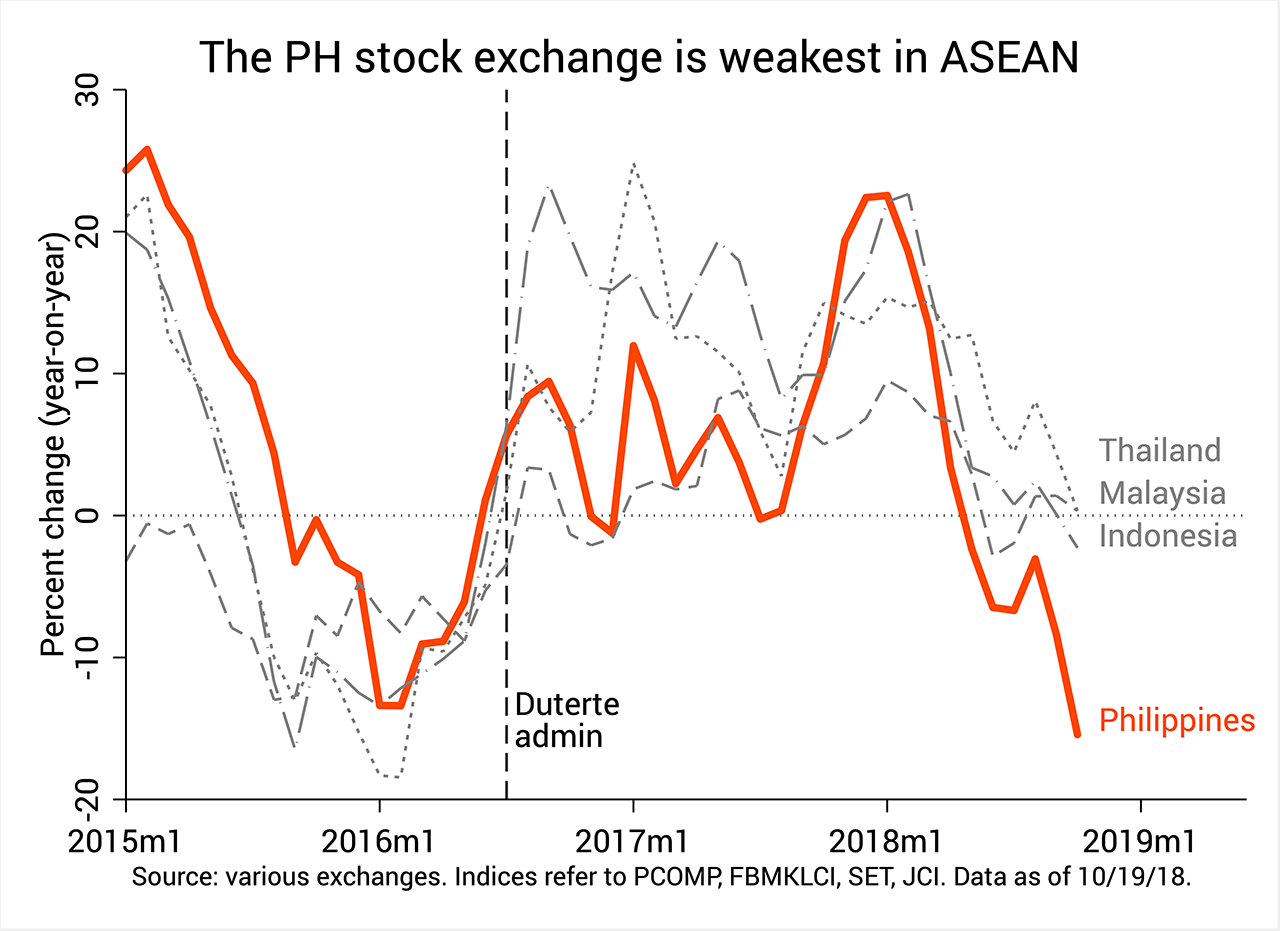

Figure 1 shows that the PSEI fell by more than 15.4% from October last year. By contrast, Indonesia’s stock index fell by 2.3% only, while Malaysia and Thailand’s indices actually rose by 0.33% each.

While all 4 ASEAN stock markets plummeted since early 2018, the Philippine market by far plunged the most. How come?

Figure 1.

What are stock markets?

To appreciate these trends, recall what stock markets do in the first place.

Stock markets are essentially collections of buyers and sellers of “stocks,” or claims to the ownership of certain companies.

People buy stocks of a company when they feel reasonably confident in that company’s future performance (as measured, say, by expected profits).

Meanwhile, they sell stocks if the company’s prospects are not very good.

The demand and supply for a particular stock determine its price. Although different stocks have different prices, you can combine them all in an “index.”

In the Philippines, the predominant stock market index is the PSEI, which comprises the stock prices of some of the country’s largest companies, such as SM Investments, Ayala Land, PLDT, Globe Telecom, Megaworld, and DMCI. Stocks of larger companies have larger weights in the index.

The daily ups and downs of the stock market index – commonly reported in the news – are important insofar as they reflect the prevailing sentiments and outlooks of the buyers and sellers of stocks.

A climbing index signals general optimism among them, whereas a dropping index signals general pessimism.

Note, however, that such movements do not reflect the sentiments of the population at large (for that, you need to look at other indicators).

International factors

The recent slump of the PSEI is largely a confluence of international and domestic factors.

It so happens that many stock markets worldwide – especially in so-called “emerging markets” (or EMs) like the Philippines – have taken a hit.

This is because the US economy has gotten much healthier since the global financial crisis, which started in 2008.

So healthy, in fact, is the US economy that the Federal Reserve has raised interest rates 8 times since late 2015 to temper US growth and combat the extra inflation it has generated.

This policy is sometimes called “taking away the punchbowl just as the party gets going.”

Higher interest rates, in turn, make it more attractive for investors to place their money in US stocks, thus prompting investors in emerging markets to withdraw their funds and migrate to the US instead.

In the Philippines, foreign investors have withdrawn as much as $1.6 billion this year (up until early October).

Aside from this massive “EM selloff,” another factor that sent ASEAN stock markets in the doldrums of late is the burgeoning US-China trade war.

This looming conflict has spooked investors about the profitability of companies in emerging markets, especially those which rely a lot on imported Chinese goods.

Domestic factors

But these international factors don’t yet explain why the Philippine stock market is today the world’s worst. What domestic factors could explain this?

For one thing, many consumers, investors, and entrepreneurs are becoming increasingly jittery about the Philippines’ economic prospects.

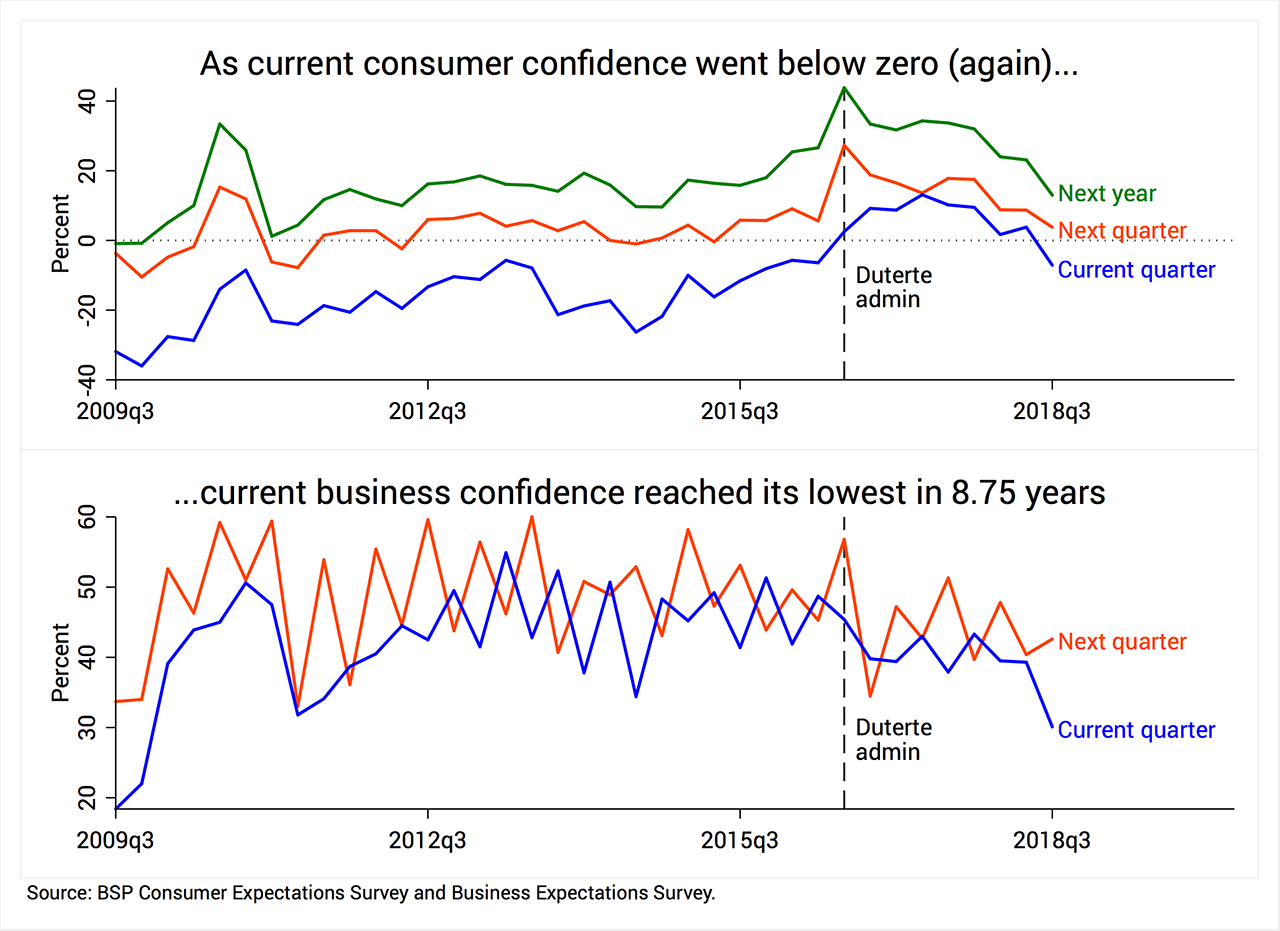

The data bear this out. Figure 2 shows that, as of July, consumer confidence reached negative levels again – the first time since Duterte came into office – while business confidence is at its lowest in almost 9 years.

Figure 2.

One major reason for this is that the Duterte government has miserably failed to rein in inflation in recent months, now at its highest in almost 10 years.

Unfortunately, inflation might climb further, what with the petroleum excise taxe hike to be imposed by the TRAIN law on January 1, 2019.

This policy – which more politicians now want to stop because it threatens their reelection bids next year – is over and above the steady rise of world oil prices.

Runaway inflation is also threatening our economic growth prospects.

Not only does inflation douse consumption spending (people are less willing to spend a lot when prices are skyrocketing), but inflation also prods the Bangko Sentral ng Pilipinas to raise its interest rates further, thus dissuading lots of people from taking on loans for their household or businesses in the future.

Duterte’s economic managers are aware of this emergent threat to economic growth. They have, in fact, recently lowered their growth targets for 2018, from 7%-8% to just 6.5%-6.9%.

But perhaps the biggest problem today is a gnawing sense of uncertainty that envelops the country, thanks to Duterte’s arbitrary policies and his lack of reliable economic leadership.

Recall that in the past two years Duterte has “weaponized” laws and regulations against certain businesses, and this rippled in the stock markets. For instance, ABS-CBN’s stock price visibly suffered when Duterte threatened to block the renewal of its franchise.

Duterte has also demonstrated his incapacity to draw up concrete and decisive solutions to the country’s biggest economic challenges (say, inflation or the rice crisis).

Most worrisome, perhaps, is the Duterte government’s penchant to put on the table such sweeping and encompassing measures that could disrupt the economy.

For example, many groups – including some government agencies like the Philippine Economic Zone Authority (PEZA) – fear the Trabaho bill could drive many investors away from the country.

The infrastructure push called Build, Build, Build, meanwhile, could heat up the economy and further weaken the peso, what with its massive import requirements.

Finally, federalism via charter change could cause total economic upheaval across the country by blowing up the country’s finances and raising the cost of doing business nationwide (among other things).

Until the government can credibly promise that these policies will not substantially undermine the economy, the private sector will remain on edge about the country’s prospects in the time of Duterte.

Uncertain times

All in all, spells of uncertainty – both international and domestic – seem to explain why our stock market is one of the world’s worst-performing this year.

Though many other emerging markets are also afflicted by the global slump, the Philippines stands out because of our own host of economic problems, notably accelerating inflation amid slowing growth.

What we need now, most of all, is to bring back a climate of stability and predictability that could dispel the pall of uncertainty now hanging over all our heads.

But can we even rely on the Duterte government to do that? – Rappler.com

The author is a PhD candidate at the UP School of Economics. His views are independent of the views of his affiliations. Follow JC on Twitter (@jcpunongbayan) and Usapang Econ (usapangecon.com).

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.