SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[ANALYSIS] Golden age? Inflation reached 50% during the Marcos regime](https://www.rappler.com/tachyon/r3-assets/D4449ECDD95448E5A220814FE63F79E2/img/445DED191B43480F8FA5D7A209B63BFA/Marcoss-50.3-inflation-rate-Sept-21-2018.jpg)

Today, September 21, is as good a time as any to look back at the deleterious economic impacts of the Marcos regime.

I wrote before that, viewed from the lens of various economic data, the Marcos years can hardly be called the country’s “golden age.” In fact, during that time, we experienced the country’s worst economic downturn since World War II. (READ: Marcos years marked ‘golden age’ of PH economy? Look at the data)

But one other aspect I haven’t yet explained is that the regime also saw the country’s highest inflation rate (inflation being an economic statistic that measures how fast prices are rising).

This is especially relevant now since inflation in August 2018 was the highest in over 9 years and the highest in ASEAN.

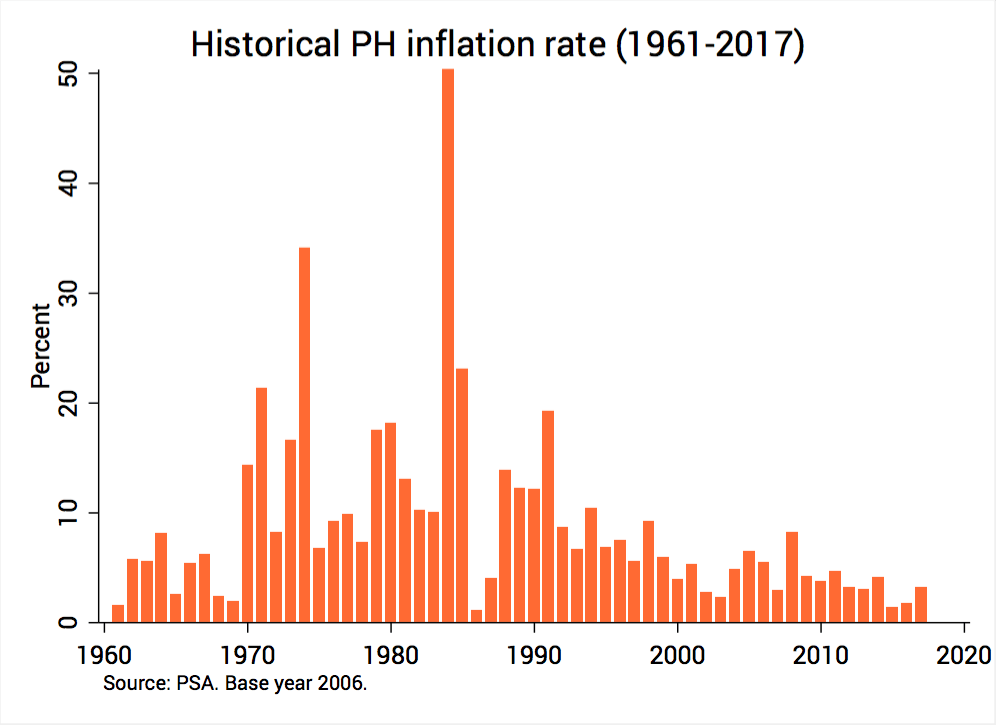

Some have tried, in fact, to belittle this recent rise of inflation by saying it’s hardly the worst we’ve had in history. This claim is corroborated by data: inflation even peaked at 50.3% in 1984 (see Figure 1). Hence, some say 6.4% is nothing to bemoan.

Figure 1.

But this is a poor way to justify recent inflation: the government’s inflation target this year is 2% to 4%, not 50.3%.

Why, though, did inflation reach a whopping 50.3% in 1984? What circumstances led to such a ridiculously high inflation rate?

Defending the exchange rate

To understand this, we have to zero in on the link between inflation and the exchange rate.

Bear in mind that we pay imported goods in foreign currencies like the US dollar. So when the peso weakens (say, from P50 to P54 per USD), we have to pay more pesos for the same amount of imports. These goods fetch higher prices and thus stoke domestic inflation.

The main difference in the 1950s and 1960s, however, was that the government then actively pursued a “fixed exchange rate.”

This means that, rather than allow the peso-dollar exchange rate to fluctuate freely according to the law of supply and demand, the government intervened in the market and tried its very best to fix it at a certain level.

A fixed exchange rate was desirable then because of the government’s overarching industrial policy, called “import substituting industrialization” (ISI). In essence, ISI fueled domestic industry and manufacturing primarily through the importation of raw materials, parts, and components.

By making the peso artificially strong, a fixed exchange rate made imports artificially cheap, thus facilitating ISI.

But maintaining a fixed exchange rate was no mean feat. To achieve this, government had to force exporters to surrender their dollar earnings to the government, a policy that prevailed from 1949 up to 1961 and was widely viewed by exporters and other business owners as unfair and heavy-handed.

Thus, there was pressure for government to pursue exchange rate “decontrol,” and President Macapagal pursued this (albeit only partially).

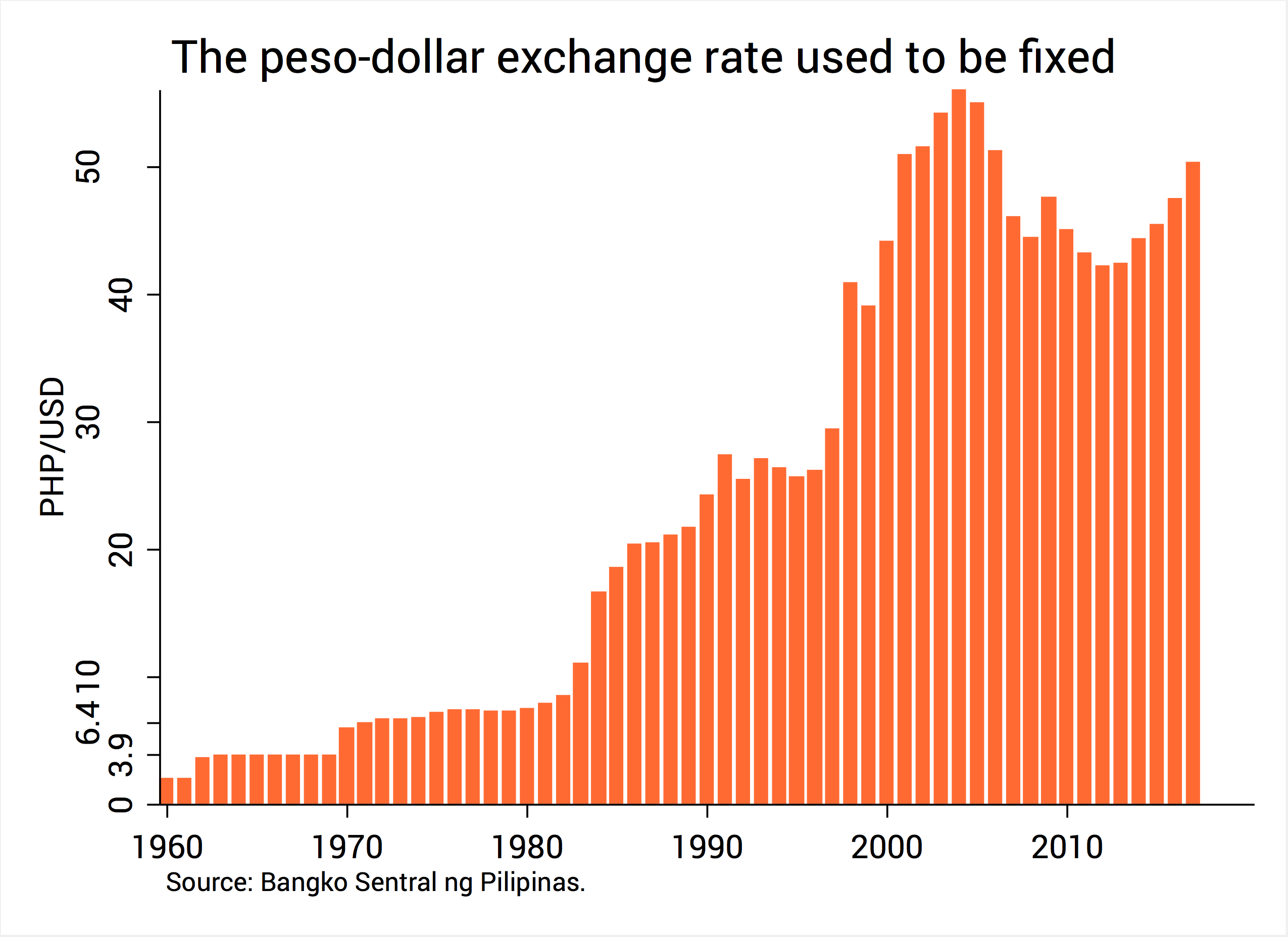

Figure 2 shows the historical peso-dollar exchange rate. Notice that from P2 per USD in 1961, the exchange rate was “devalued” to P3.9 per USD in 1962.

Figure 2.

But the peso’s sudden devaluation – although seemingly small – stoked inflation and made life harder for Filipinos. Inflation was just 1.6% in 1961, but it rose fivefold to 8.2% by 1964. At the same time, exporters were clamoring for full decontrol, rather the partial one Macapagal implemented.

Enter then-Senate president Ferdinand Marcos, who latched onto this economic debate and decried the inflation induced by Macapagal’s devaluation.

Long story short, Marcos successfully turned this economic issue into a political one, and this helped to pave his own path to the presidency in 1965.

Double-digit inflation

But things were no better during Marcos’s time. In fact, things took a turn for the worse.

In Figure 1, notice that inflation reached double-digits during the Marcos years: it peaked in 1971 (21.4%), in 1974 (34.2%), and again in 1984 (50.3%). Why?

For one thing, Marcos pursued massive government spending since his first term (1965 to 1969). He also continued the protectionist industrial policies of the past, which implied that imports remained well in excess of exports.

Both these strategies depleted our foreign currency reserves to alarming levels in the late 1960s. This deterioration could have been abated if the peso were free to adjust according to supply and demand. But then it was still adamantly fixed.

Hence, there was mounting pressure for government to abandon the fixed exchange rate.

Ultimately, government succumbed. Our fast-depleting reserves could only be replenished by borrowing from the International Monetary Fund (IMF), but they would lend only if the Philippine government devalued its peso once more.

Thus, in Figure 2, you see that the exchange rate changed from P3.9 to P6.4 per USD in 1970. At the time government also abandoned a fixed exchange rate regime in favor of a “managed float,” where the exchange rate was allowed a little room to fluctuate.

However, just like in 1962, this devaluation – along with a slew of devastating typhoons – led to an inflation spike: inflation reached its first double-digit level at 14.4% in 1970, followed by 21.4% in 1971.

Inflation would peak again at 34.2% in 1974, but this was largely because of skyrocketing world oil prices.

Debt moratorium

But what really led to the historically high 50.3% inflation rate in 1984 was the country’s worst postwar economic crisis, brought about by Marcos’ pernicious policy of debt-driven growth and crony capitalism.

There’s no space here to give justice to the details of the Marcosian economic crisis (a good place to start is the 1984 “white paper” of UP School of Economics faculty members).

But it will suffice to say that we came to a point where we buried ourselves in so much debt that we just said in 1983 we couldn’t pay any of it (a so-called “debt moratorium”).

This, of course, did not reflect well on our global standing as a borrower, and no lender dared touch us with a 10-foot pole.

We had no choice but to secure another round of emergency funds from the IMF, but this time they were stricter and lent only on the condition of a painful – if harsh – devaluation of the peso. Hence, the movement from P10 to P14 per USD in 1983.

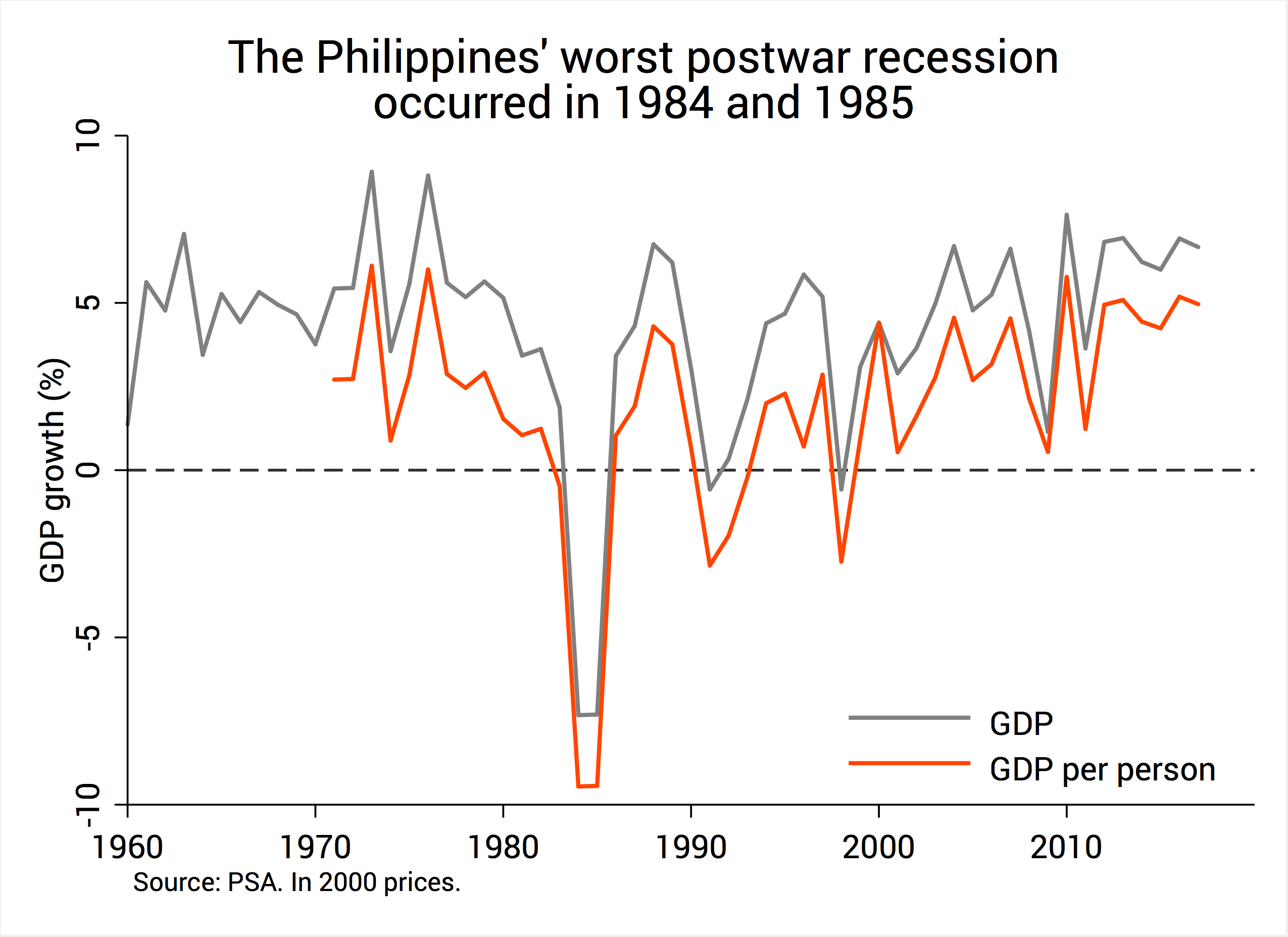

The paucity of foreign currency reserves meant we could import but a few capital goods from abroad. Together with the inevitable rise on interest rates (which further stifled economic activity), this precipitated the country’s worst postwar recession, where the economy contracted by 7% for two straight years, in 1984 and 1985 (Figure 3).

Figure 3.

This episode of stagnation and high inflation – also called “stagflation” – was a double whammy, a perfect economic storm from which Filipinos’ average incomes didn’t recover until two decades later.

Does anyone still think that this era was the Philippine economy’s “golden age”?

Debunking the myths

Record-high inflation in 1984 was just the tip of the iceberg that was the Marcosian socioeconomic crisis.

The spike in poverty and underemployment, the wanton disregard for human lives and human rights, the erosion of democratic institutions, and the wide-scale corruption of both the public and private sectors – all these belie claims that the Marcos years marked the country’s “golden age.”

And yet, sadly, such myths persist today. This is evidenced by the proliferation of online memes, textbooks that whitewash the Marcos regime, or the near-win of Bongbong Marcos in 2016.

The last thing the country needs right now is a return of the Marcoses to Malacañang. One way we can prevent that is by tirelessly debunking the Marcosian economic myths.

It may also be the easiest: we have the data firmly on our side. – Rappler.com

The author is a PhD candidate at the UP School of Economics. His views are independent of the views of his affiliations. Follow JC on Twitter: @jcpunongbayan.

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.