SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

WASHINGTON, USA – A key US banking regulator on Monday, May 1, laid out a range of options for reforming the federal deposit insurance system and concluded that significantly increasing the backstop for bank accounts used for business purposes was the “most promising.”

In the wake of March’s lightning-fast bank failures, expanding coverage for accounts used to cover payroll, invoices, and other large business transactions has emerged as the Federal Deposit Insurance Corporation (FDIC)’s preferred route for balancing financial stability and depositor protection, relative to its cost.

In order to effect any change to the government deposit protection scheme that has largely remained intact since its debut in the Great Depression in the 1930s, Congress would need to write a new statute describing what types of accounts would receive any additional coverage, FDIC officials said during a briefing with reporters.

The 76-page report also considered backstopping all accounts no matter what the amount, an option that would do the most to prevent bank runs, the report said, but would also have significant implications for market disruptions and could increase bank risk-taking.

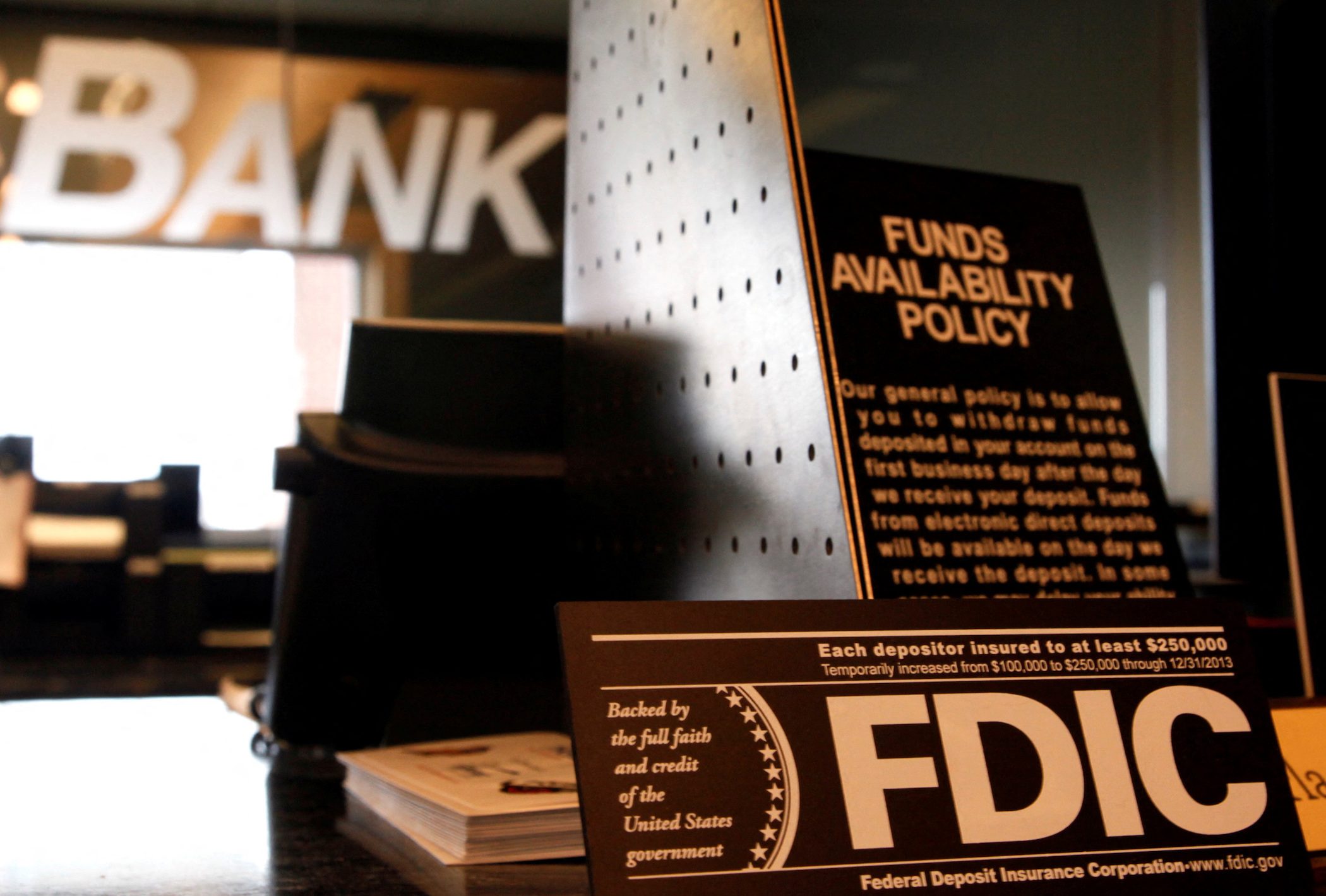

Keeping the current system, where coverage is limited to $250,000 per person per bank, was the third option considered. While it would entail the least market disruption, it “fails to address the financial stability challenges” of large concentrations of uninsured deposits, the report said.

FDIC Chair Martin Gruenberg asked staff to undertake an analysis and review of options for reform of the deposit insurance system after the collapse of Silicon Valley Bank (SVB) and Signature Bank in March, when regulators ended up backstopping all deposits to prevent contagion to the banking system.

Deposits at First Republic Bank, which was seized by regulators on Monday and sold to JPMorgan Chase & Co., did not require any formal government backstop, though the FDIC said the transaction would cost it $13 billion, on top of the $22.5-billion hit it has already taken from the SVB and Signature Bank failures.

The FDIC’s deposit insurance fund helps to fulfill the agency’s guarantee of bank deposits up to $250,000 per person. In the event an insured bank fails, the FDIC uses the deposit insurance fund to pay back customers who maintained accounts under the limit.

That $250,000 limit was enshrined in law by the 2010 Dodd-Frank reform law passed following the 2008 financial crisis, upped from what was before a $100,000 cap.

But following the collapse of SVB and Signature, there have been calls for a rethink.

Some 99% of US bank accounts are fully insured under current FDIC limits. But uninsured deposits have grown rapidly in recent years, tripling since 2009 to $7.7 trillion. Large concentrations of uninsured deposits increases the potential for bank runs and can threaten financial stability, as was seen with SVB and Signature, both large banks with more than $100 billion in assets.

But even banks that many would consider midsized or small have become heavily reliant on easily runnable uninsured deposits, the report showed: more than half of deposits at 40% of banks with assets of $57 billion are uninsured.

Some of the increase, the report noted, may be a temporary effect of the deposit surge from COVID-19 pandemic government aid. But to the extent those large deposits are payroll or other business payment accounts, the report said, they may be “relatively more sensitive to adverse developments affecting banks.”

An insurance scheme that would give such business accounts greatly increased or even unlimited coverage could enhance financial stability by making it much less likely those depositors would flee a bank en masse.

But it would also have challenges, the report said, including defining what accounts qualify and keeping depositors and banks from trying to circumvent the rules and obtain coverage for which they shouldn’t be eligible. It would also likely cost more, with higher assessments levied on banks, the report said.

US Federal Reserve Chair Jerome Powell told Republican lawmakers in March that Congress should reevaluate limits on the size of federally insured bank deposits.

Democratic Senator Elizabeth Warren told CBS’ Face The Nation in March that lifting the cap would be “a good move,” and Republican Senator Mike Rounds has questioned whether the $250,000 limit is still appropriate.

An explicit guarantee

Those in favor of getting rid of the cap argue that the government’s full backstop of SVB and Signature deposits already signals an implicit guarantee of all bank deposits.

Eliminating the cap altogether could be expensive and could end up undermining financial stability, the report said, because banks might take greater risks if their deposit bases are considered more stable.

Any changes would need legislation from a deeply divided Congress. The Republican House Freedom Caucus said in a March statement that its members would oppose any universal federal guarantee on bank deposits above the current $250,000 limit. – Rappler.com

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.