SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

I was jogging once in our village, mulling over how best to manage our family’s resources: our income, savings, needs, and some wants as well.

As I pondered on it, it increasingly felt like there was a tug-of-war going on in my head: I want this but I need that; this is nice, but that is more essential.

More often, it is a struggle between compulsion and reason, between what is rational and what is emotional.

Truth be told, compulsion and emotion have their own days, much to reason’s regret after.

So how do I prioritize my expenses? Surely I don’t want to be deprived, but I do want a comfortable future as well. Thinking more along these lines, I have seen that the battle lines are drawn between wants and needs, between present and future.

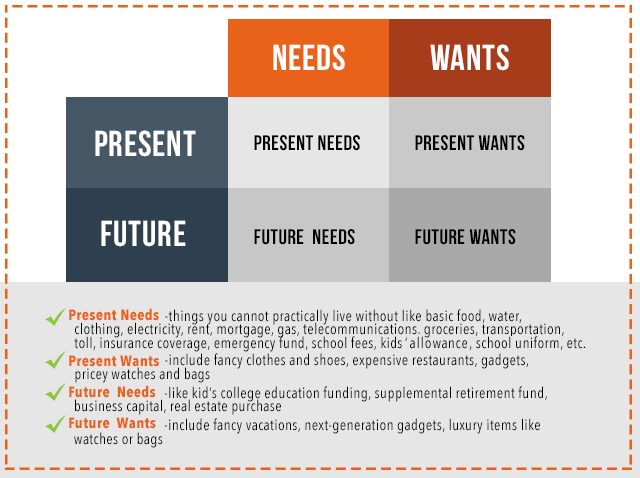

Then it hit me like lightning. You can make a quadrant out of them! Combining all, you have:

You can classify your goals and dreams into these 4 basic categories, making it easier to prioritize. Try it!

Ideally, the order of priority should be as follows:

- Present Needs

- Future Needs

- Present Wants

- Future Wants

Number 1 is definitely non-negotiable. These are essentials and should be first in your cash allocation.

Numbers 2, 3, and 4 are a bit more tricky – you can allocate for some present and even future wants, as long as these do not severely impair your future needs. Going to a beach resort, getting pampered at a spa, or even buying a fancy bag can be okay, as long as you are still able to fund your future needs.

Imagine always setting aside money for the latest gadget, but having nothing for your child’s college education. How about driving the latest, most expensive car, but having an empty retirement fund? (The money for your car can already be your retirement fund!) Or sporting a luxury watch, yet having no insurance protection for your family? How would that speak of your priorities?

Again, this is not to say that we should all live a dry, deprived life. If you can afford and fully fund everything, then go ahead. For instance, if you have P30 million in cash, I don’t mind you sporting a Rolex. But if you sport one and you only have P100,000 in your asset column, then we have a problem.

Managing one’s finances is indeed tricky. It’s a slippery slope, and once you slip, it could be very difficult to recover. The key is really to stay focused on your financial goals.

So, are you ready to make your own financial quadrant? – Rappler.com

Rienzie P. Biolena is a registered financial planner of RFP Philippines, a professional group of financial planners in the country. To learn more about RFP, you may email info@rfp.ph.

Rienzie is also an accredited investment fiduciary of Pennsylvania-based fi360 and an international member of the Financial Planning Association, the largest association of financial planners in the US. You may reach Rienzie at rienzie.biolena@gmail.com, his Facebook account, or on Twitter (@rbiolena).

Balancing beam image from Shutterstock

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.