SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[ANALYSIS] Why is Philippine inflation now the highest in ASEAN?](https://www.rappler.com/tachyon/r3-assets/4A0970D12C774D96850FBCDB5D2707AA/img/F69263167B7D4175BD4F91C9B6AB3F92/Why-is-Philippine-inflation-now-the-highest-in-ASEAN.jpg)

Yesterday, we were greeted by truly shocking news: the Philippines’ inflation rate, which measures how fast prices are rising, reached a whopping 6.4% in August.

Not only is this the highest in 9.4 years, it also exceeded the government’s upper forecast of 6.2%, and is way above the government’s 4% upper target for 2018.

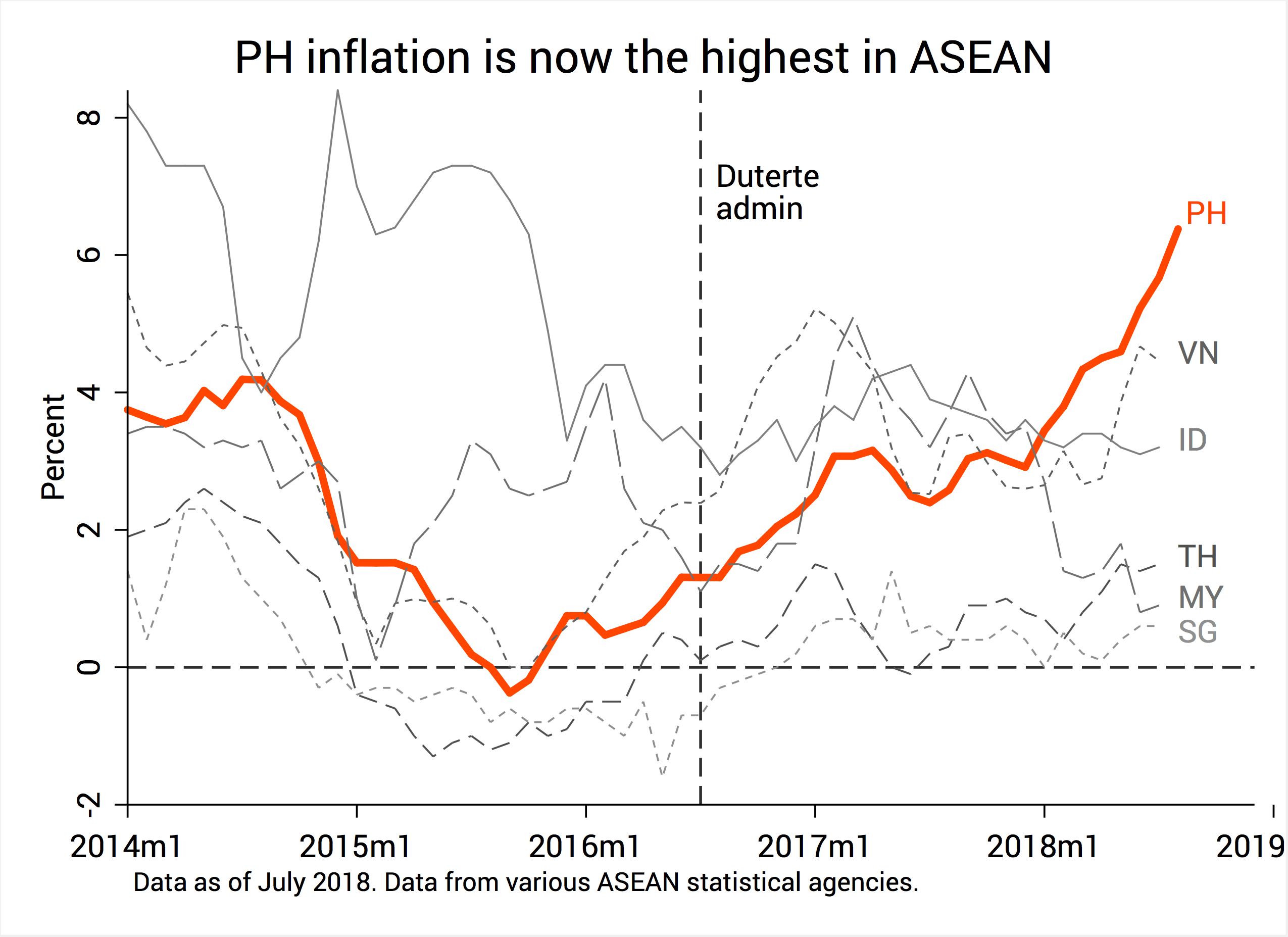

Data also show it’s now the highest in all of ASEAN. Figure 1 shows that Vietnam’s inflation rate (at least as of July) was only at 4.5%, Indonesia 3.2%, Thailand 1.5%, Malaysia 0.9%, and Singapore 0.6%.

Notice too that when President Duterte came into office, Philippine inflation can be found right in the middle of the ASEAN pack. These days, we’re on top of everyone else.

But why is inflation running away in the Philippines and not in other ASEAN countries?

Figure 1

World oil prices

Inflation is always going to be a mix of international and domestic factors.

One obvious suspect is the continuing rise of oil prices worldwide.

Countries with no substantial oil production to speak of – like the Philippines – are forced to import oil. Consequently, they are at the mercy of global oil price movements determined largely by supply and demand.

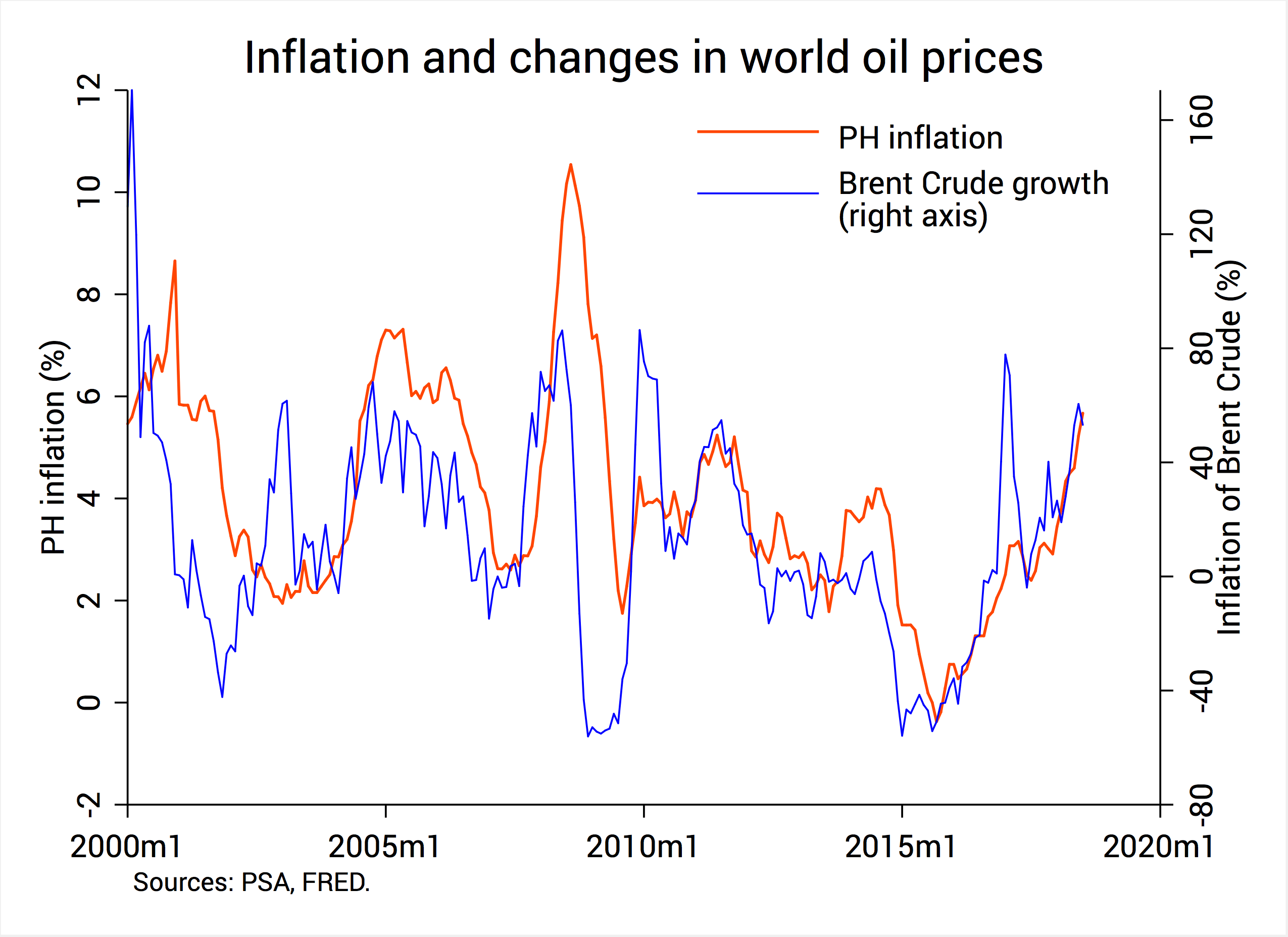

Figure 2 shows the close correlation between domestic inflation and the yearly changes in global oil prices. Based solely on this graph, you might be forgiven to think world oil prices alone can explain much of the changes in Philippine inflation.

Figure 2. A similar graph was made by Jun Neri using WTI Crude instead of Brent Crude.

One possible reason for this pattern is that the Philippines is one of the biggest net importers of oil in ASEAN.

One study showed that, back in 2016, we imported as much as 94% of our oil requirements, vis-à-vis Thailand which only imported 70%, Indonesia 41%, Vietnam 20%, and Malaysia 10%.

If indeed valid, this theory gives us reason to think President Duterte’s tax reform law (TRAIN) is patently ill-timed.

If you recall, TRAIN included tax hikes on several petroleum products, such as unleaded gasoline, diesel, and kerosene. Unknown to many, TRAIN also provides for two more rounds of automatic petroleum tax hikes in 2019 and 2020.

This policy, to me, is like rubbing salt on one’s economic wounds.

Combined with the fact that global oil prices later this year could reach up to $90 per barrel—because of limited supplies from key oil exporters like Iran and Venezuela—it seems cruel to impose additional tax hikes on fuels come January 2019.

Therefore, the proposed bill to stop the implementation of TRAIN’s petroleum tax hikes seems more and more justified by the day – if only as a stopgap measure to arrest runaway inflation immediately.

Weak peso

Another factor that contributes to runaway inflation is the weakening peso.

As of September 5 the peso closed at P53.5 per US dollar, the lowest it’s been in 12.2 years. The peso is also one of the weakest currencies in ASEAN today.

Because we pay imports in foreign currencies, a weaker peso necessarily makes imports costlier. As such, oil becomes costlier too, as well as all the other goods and services in the economy that rely on it.

But why is the peso slumping to begin with?

I argued before that perhaps the largest reason is a domestic one: imports are experiencing double-digit growth rates, even as exports have shrunk for 6 consecutive months.

This widening “trade gap” roughly means we’re shelling out more dollars than we are earning, and the relative abundance of pesos in the local market robs it of its value.

Note that a lot of such imports are raw materials (like iron and steel) and capital goods meant for Duterte’s infrastructure push called Build, Build, Build. Therefore, you can say that Build, Build, Build is partly to blame for the weaker peso.

This is not necessarily bad. But insofar as a weak peso makes imports costlier in general, then Build, Build, Build also sows the seeds of future inflation.

People’s expectations

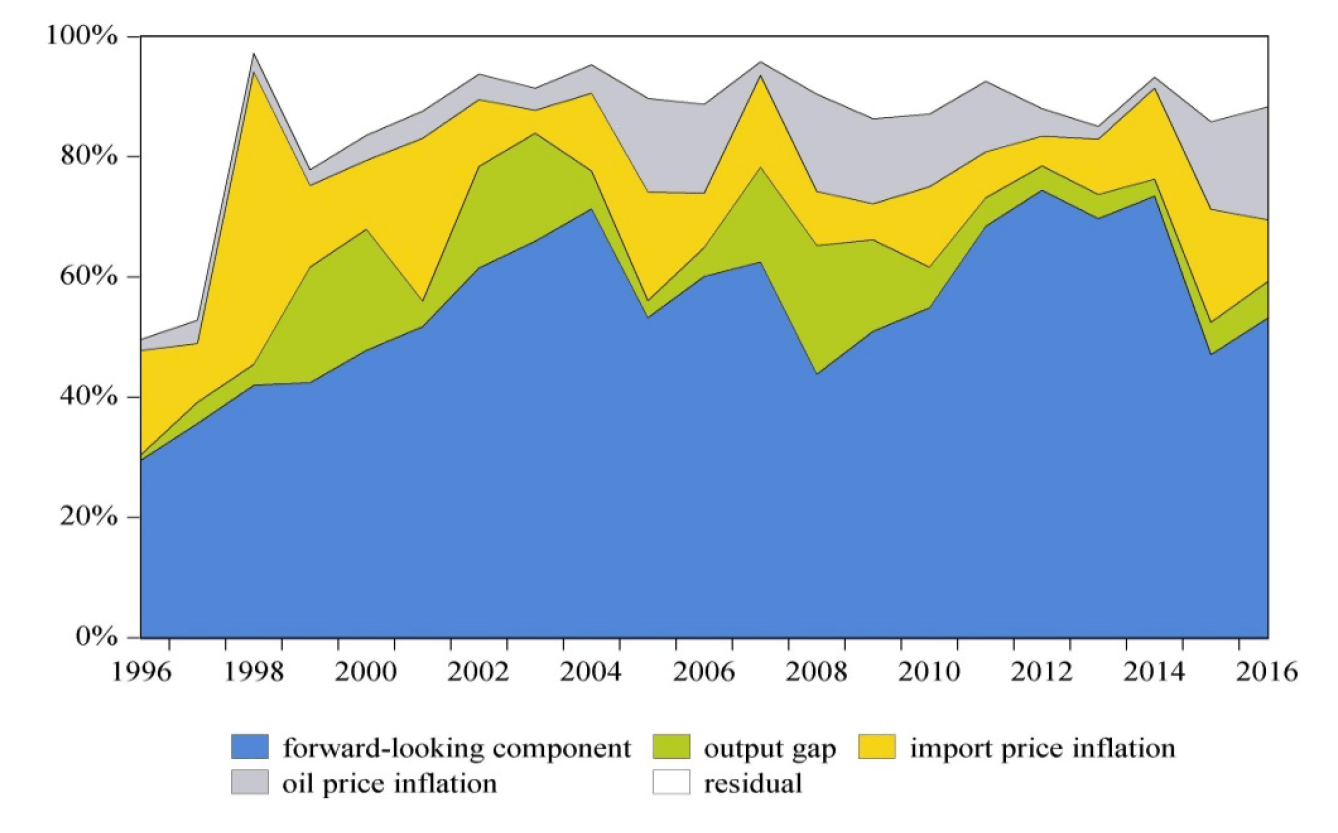

But perhaps the biggest – and most underappreciated – factor behind inflation is people’s expectations of inflation.

A recent study by IMF researchers, for example, shows that at least half of inflation in ASEAN-5 countries is attributable to how people anticipate future inflation. This factor (the blue area in Figure 3) overwhelms all other factors such as oil and import prices.

Figure 3. Relative contributions to inflation in ASEAN-5 countries. Source: Dany-Knedlik and Garcia [2018].

Figure 3. Relative contributions to inflation in ASEAN-5 countries. Source: Dany-Knedlik and Garcia [2018].

Inflation expectations matter because they change how people behave.

For example, if news outlets announce that oil companies will hike gasoline and diesel prices at midnight tomorrow, consumers today will race to the gas stations to fill up, spiking demand and stoking prices further.

This mentality applies to inflation as well. If people expect inflation to rise in the coming months, not only will consumers hoard basic goods, but workers will also lobby for higher wages, and firms will also revise their menus or price lists to safeguard their profits.

All these effects add up to further inflation. In this sense, the original expectations become “self-fulfilling prophecies.”

It’s in government’s interest, therefore, to manage (or “anchor”) people’s inflation expectations from time to time.

If, say, the government wants inflation to fall between 2% to 4% from 2018 up to 2020, then government must ensure this is credible. For that to happen, the people must see that government is on top of inflation.

For its part, the Bangko Sentral ng Pilipinas already raised its key interest rate in recent months: by 0.25 percentage point in May and June, and by 0.5 percentage point in August. Many analysts expect another big rate hike this month.

Some people have argued that this “tighter” monetary policy came in a tad too late. Still, others worry that this won’t do much anyway because monetary policy usually operates with a long lag, and recent inflation is largely supply-driven (rather than demand-driven).

Rice crisis

Finally, domestic inflation has also been boosted by tighter supply of many agricultural products, notably rice.

Last week I wrote about the burgeoning rice crisis. Since then, President Duterte has flatly denied there’s any problem. Agriculture Secretary Manny Piñol also laughably ate weevil-infested rice on national TV, as if that will do anything to cover up the bungling policies of the National Food Authority (NFA).

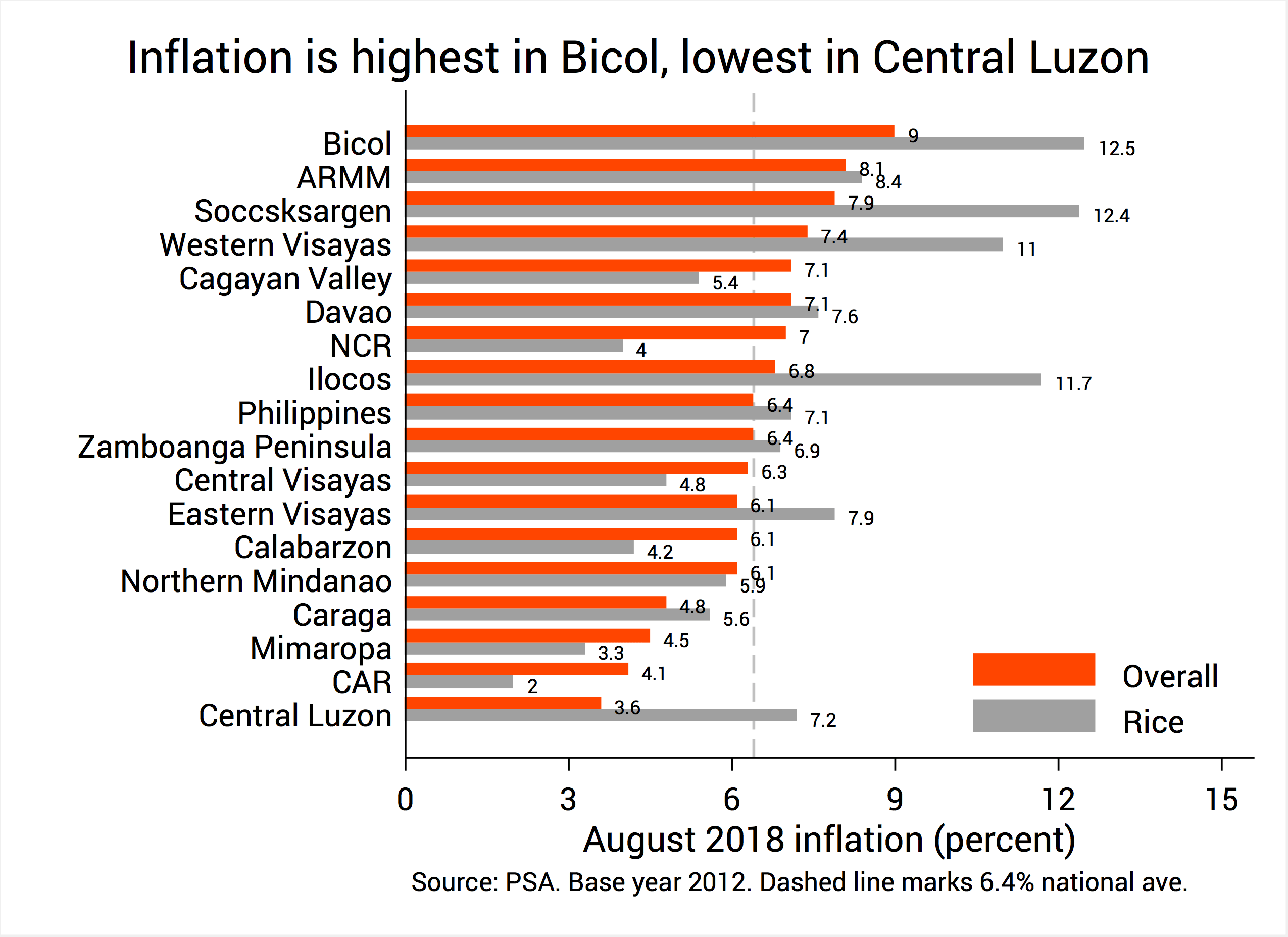

What’s not laughable is the fact that some regions have experienced double-digit rice inflation rates last month (see Figure 4). The situation is direst in Bicol, which not only suffered the highest regional inflation rate (9%), but also the highest rice inflation rate (12.5%).

Figure 4

It’s not just rice, by the way. Vegetables inflated by 19.2%, corn 12.6%, fish 12.4%, and sugary goods 9.1%. For these products, there are regional variations as well.

What to do? At least for rice, government can mop up its errors by importing more rice, fast-tracking the distribution of imported rice, and passing the rice tariffication bill.

Duterte will also do us all a favor by immediately firing the inept officials who brought about this needless rice crisis, namely the NFA Administrator and the Agriculture Secretary. Duterte might also consider abolishing the NFA for good.

This is not fine

By and large, August’s 6.4% inflation rate surprised everyone, not least the economic managers.

The first order of business is to arrest inflation immediately. The economic managers can do this by decisively halting TRAIN’s petroleum tax hikes next year, further raising interest rates, and hastening the importation and distribution of rice nationwide.

More importantly, however, the economic managers must rein in people’s expectations about future inflation. They can do this by regaining the people’s trust and showing us all they’re on top of the economic situation.

They can’t do this by continuing to deny there’s a problem. In the wake of the 6.4% inflation announcement, for example, Socioeconomic Planning Secretary Ernesto Pernia said it’s “not alarming” and “quite normal in a fast-growing economy.”

It’s one thing to remain calm in the face of a crisis. It’s another to flatly deny there’s a problem, even if it’s already staring you in the face.

The economic managers’ blithe remarks about inflation call to mind the famous “This is Fine” meme circulating the net, where a humanlike dog, sitting in a room engulfed by flames, sips coffee and tells himself, “This is fine.”

Needless to say, our present economic situation is not fine. Our economic managers will do well to acknowledge the flames around us before things are too late. – Rappler.com

The author is a PhD candidate at the UP School of Economics. His views are independent of the views of his affiliations. Follow JC on Twitter: @jcpunongbayan.

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.