SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

MANILA, Philippines – In this year’s World Competitiveness Yearbook (WCY), the Philippines climbed 5 notches compared to 2012, from 43rd to 38th (ranked out of 60 countries).

Optimism is high in the business sector—the highest it has ever been since the Bangko Sentral started monitoring over-all business confidence in 2006. Of course, recent election spending may have contributed, but so too did the investment grade credit rating from Fitch Ratings, Standard and Poor’s and Japan Credit Rating Agency.

International observers are recognizing the achievements of the country, in terms of disaster resilience and tourism promotion. Favorable international conditions (including rising costs in China and the adjustments in Japanese-led global production networks) are opening opportunities for Philippine manufacturing—the so-called missing middle sector in our economy. And this renaissance is something reformers now want to build on.

The litany of challenges, however, remains almost unchanged. Growth will most certainly hit the wall, if more robust energy and infrastructure investments are not forthcoming. And the benefits of any growth that does occur will still remain concentrated in the hands of a few if deep structural reforms are not pursued.

Ultimately what the economy may need now is a “big push” to spur investments, promote stronger competition, and trigger massive job creation.

First the good news: the Philippines is now ranked 38th in the WCY sample of 60 countries. Now the not-so-good news: we were 38th already in 2000, so we still have a long way to go.

The country has reversed an over-decade-long decline in its ranking. The Philippines is now 11th among Asia Pacific countries in the WCY sample (compared to 13th in 2009), overtaking both India and Indonesia.

Backed by a robust 6.6% GDP growth – the second highest in Asia – a soaring stock market, and an upgrade to investment grade by several major rating agencies, the Philippines has been hailed by many analysts as the next economic tiger of Asia.

| Ranking in the World Competitiveness Yearbook | ||||||

| 2000 | 2005 | 2010 | 2011 | 2012 | 2013 | |

| Hong Kong | 14 | 2 | 2 | 1 | 1 | 3 |

| Singapore | 2 | 3 | 1 | 3 | 4 | 5 |

| Taiwan | 22 | 11 | 8 | 6 | 7 | 11 |

| Malaysia | 25 | 28 | 10 | 16 | 14 | 15 |

| Australia | 13 | 9 | 5 | 9 | 15 | 16 |

| China | 31 | 31 | 18 | 19 | 23 | 21 |

| Korea | 28 | 29 | 23 | 22 | 22 | 22 |

| Japan | 17 | 21 | 27 | 26 | 27 | 24 |

| New Zealand | 21 | 16 | 20 | 21 | 24 | 25 |

| Thailand | 33 | 27 | 26 | 27 | 30 | 27 |

| PHILIPPINES | 38 | 49 | 39 | 41 | 43 | 38 |

| Indonesia | 45 | 59 | 35 | 37 | 42 | 39 |

| India | 43 | 39 | 31 | 32 | 35 | 40 |

| Source: World Competitiveness Yearbook Database | ||||||

Economic performance

The Philippines’ highest improvement in factor ranking was posted in economic performance, which jumped 11 places to 31st from 42nd.

This improvement was mostly driven by the robust 6.6% real GDP growth in 2012 – the second highest in this year’s WCY, second only to China’s. This drove the domestic economy sub-factor ranking to 32nd from 44th.

International trade also posted a solid 25-notch improvement from 55th to 30th, driven by the US$7.13 billion current account surplus and the 7.6% growth in export of goods (in US$ value) – the 6th highest in WCY. (We must note here, of course, that the current account surplus is also due to robust remittances.)

Foreign Direct Investments

On the other hand, in spite of the 9.8% growth in net FDI inflows in 2012 and the 42.7% increase in 2011, the Philippines slipped in the international investment sub-factor from 54th to 55th, as other competitor countries raked in significantly more FDI inflows.

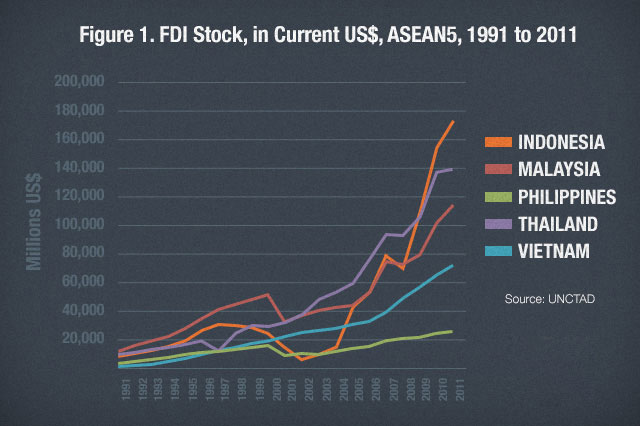

In 2012, the Philippines posted US$2.0 billion in net FDI inflows, much lower than Malaysia’s $9.4 billion, Indonesia’s $ 19.5 billion, and Thailand’s US$ 8.6 billion. The disparity in FDI achievement between the Philippines and its neighbors is better illustrated by figures on FDI stock.

The country is not only lagging behind – the gap with its neighbors is also increasing (see Figure 1).

Government Efficiency

Government efficiency slightly improved from 32nd to 31st. National government revenue increased by 12.9% in 2012, and taxes as share of GDP slightly increased to about 13% – the highest level in 5 years.

This pulled the fiscal policy sub-factor two notches up from 11th to 9th. It must be noted, though, that although tax collections improved, the two largest revenue-generating government agencies failed to reach their target collection.

The Bureau of Internal Revenue (BIR) fell short by about P8 billion while the Bureau of Customs (BOC) was almost P60 billion below target. These revenue shortfalls are not uncommon during periods of reform.

Deeper and more sustained reforms in these revenue collecting agencies may take time to bear full fruit, yet these are critically important for the longer run competitiveness of the country. Making tax payments easier through the use of IT, both for businesses and for individuals, can potentially increase tax collection, thus improving services for taxpayers while at the same time minimizing opportunities for corruption.

In addition, updating our Tariff and Customs Code (circa 1957) could also be a critical ingredient in modernizing the BOC and clarifying and updating the quagmire of rules and procedures that remain haven for rent-seeking.

Infrastructure

The Philippines dropped in the infrastructure ranking, from 55th to 57th. It is consistently the lowest-ranked factor for the Philippines, highlighting the major improvements needed in this area.

There have been recent efforts to address this, most notably the Public-Private Partnership program, but progress has been slow. In 2011, only one PPP project was rolled out (out of 10 expected) and only 8 in 2012 (out of 16 expected).

Some analysts also point out that the good fiscal performance in 2011, and to a lesser extent in 2012, was due to under-spending of the government in crucial infrastructure projects. Nevertheless, the National Economic and Development Authority (NEDA) recently stated that the government is targeting to increase infrastructure spending to 5% of GDP by the end of President Aquino’s term in 2016.

Energy

Energy remains one of the major constraints in economic development and industrialization. According to WCY data, the Philippines has the 10th highest electricity cost for industrial users among the ranked countries at US$0.18 per kilowatt hour (kWh).

This is significantly higher than Thailand’s and Indonesia’s US$0.07 per kWh, and Malaysia’s US$0.09 per kWh.

According to the Department of Energy, the installed generating capacity of all power plants in the Philippines increased by only 21% from 2001 to 2011, while real GDP grew by 61% during the same period.

Shortage in electricity supply is most pronounced in Mindanao, which has been suffering from constant power interruptions for the past several years now. Little wonder then that the region fails to attract more robust investments in sectors that require competitive energy rates.

Imbalanced growth due to imbalanced investments?

Robust growth in GDP and other economic indicators pushed the Philippines up the latest WCY ranking. But are these improvements translating to the end-goal of inclusive growth and human development?

We were given a glimpse of the answer when NSCB released first semester 2012 poverty figures based on the first round of FIES. Poverty incidence hardly moved from its 2009 level, in spite of 6% average annual GDP growth during these years.

Regional GDP figures show the imbalanced growth and development in the country. In 2011, the National Capital Region accounted for 36% of GDP but only 13% of population.

In contrast, Mindanao contributed only 14% to GDP but has 24% of population. Regional GDP per capita shows the marked difference in income across regions, with NCR having per capita GDP almost 13 times greater than ARMM.

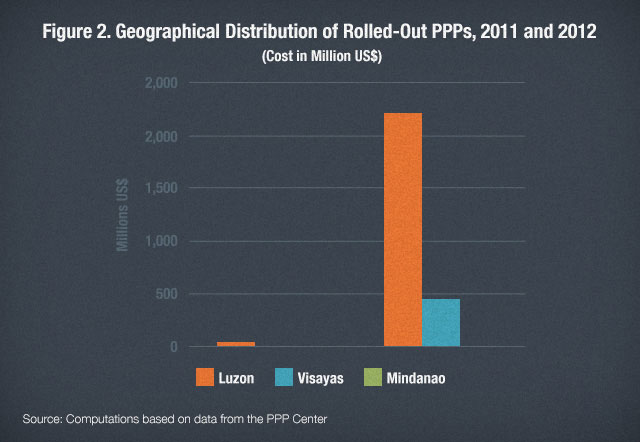

Unsurprising that imbalanced growth is shadowed by imbalanced investment and productivity. Investments in infrastructure continue to disproportionately favor Luzon, with the lion’s share of PPP projects rolled out favoring that region over more meager PPP investments in Visayas and Mindanao (see Figure 2).

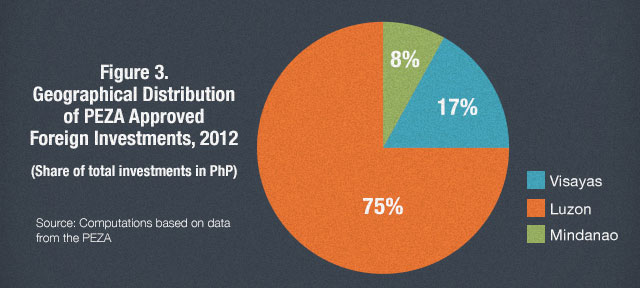

Similarly, foreign investments in Philippine economic zones also favor Luzon which accounts for over three-quarters of the total (see Figure 3).

Perhaps one of the bright spots as far as progress in promoting more inclusive investments is the government’s Pantawid Pamilyang Pilipino Program or 4Ps. With its targeted focus on children in poor families, this program seeks to improve the country’s human capital investments in the next generation.

By increasing education and health investments for these children, the program could contribute to increasing their chances of eventually successfully participating in the market economy and breaking free of the poverty trap. Unlike many other government programs that fail to be subjected to rigorous evaluation, the 4Ps has been (and continues to be) evaluated, and the emerging evidence suggests a positive impact which could be further buttressed by continuing to improve on the program.

Nevertheless, the true measure of success and permanent exit from poverty would be whether there are jobs waiting for them when they eventually enter the labor force.

Speeding up, while staying on matuwid na daan

In all the areas mentioned earlier—FDI, government efficiency, infrastructure, energy and investments (including in human capital)—it is fair to say that some progress has already been made.

However, the pace of reform, and the elements that promote stronger inclusiveness in economic outcomes could be ratcheted-up several notches.

We also need an industrial policy blueprint that will spur the “big push” that our economy needs to compete. And however this blueprint might look like, it must be potent enough to generate roughly 1 million new jobs per year, for at least the next two decades.

As we have noted in an earlier AIM Policy Center study, our forthcoming youth bulge (i.e. the share of our youth in the total population), which is projected to peak in about 25 to 30 years, necessitates this level of ambition.

Perhaps only an industrialization of this magnitude will be able to absorb roughly one-third of our (still growing) population that remains mired in poverty. – Rappler.com

*The World Competitiveness Yearbook is produced by the AIM Policy Center in partnership with IMD Business School and think tanks in 60 countries. AIM Policy Center has been tracking the Philippines’ economic competitiveness ranking since 2000. Tristan Canare co-authored sections of this article. Questions and comments on this article could be addressed to: policycenter@aim.edu.

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.