SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

About six months before Credit Suisse was sold to rival UBS in a weekend rescue, the head of the Swiss central bank wanted to inject 50 billion Swiss francs ($57.6 billion) into the lender and nationalize it, according to three sources with direct knowledge of the matter.

Hobbled by a series of scandals and failed restructuring plans under successive management teams, Credit Suisse had experienced massive deposit outflows in October 2022. Swiss National Bank (SNB) Chairman Thomas Jordan and other officials believed the lender faced an existential crisis that could not be solved by just injecting cash, two of the sources said.

Nationalizing the bank would have allowed regulators to install new managers who could restore confidence, one person with knowledge of the matter said.

But Switzerland’s financial regulator FINMA and the finance ministry opposed the idea, as did Credit Suisse’s management, the sources said. Unable to agree, Swiss authorities decided the best solution was to let the company find its own way, the three sources added.

The episode, many details of which are reported here for the first time, was one of several points of friction among Swiss officials in recent years over how to regulate the country’s banks, including how much deference to give management teams.

Interviews with more than two dozen people, including current and former officials, industry executives, and advisers, show those differences undermined the ability of Swiss regulators to properly oversee Credit Suisse, which became the first systemically important bank to collapse since the financial crisis of 2008.

Amid the lax oversight, Credit Suisse hurtled from one scandal to the next. Taken together, that meant when the lender in effect became insolvent in March due to a run on deposits, Swiss authorities were unprepared and had only one realistic option: to sell it to rival UBS, supported by more than 200 billion francs in state-funded guarantees, the interviews show.

Credit Suisse’s demise tainted Switzerland’s reputation as a major center of world finance and a safe haven, and debunked the belief that global banks are safer now.

Better understanding of what happened can help strengthen global financial regulation and hold Swiss regulators accountable now that they oversee an even bigger bank: after acquiring Credit Suisse, UBS has a balance sheet of more than $1.6 trillion, nearly twice the size of the Swiss economy.

“Many people here feel that it would’ve been much better if policymakers had acted much earlier,” said Stefan Gerlach, chief economist of Switzerland’s EFG Bank and former deputy governor of Ireland’s central bank. “One element common to many financial crashes is that politicians are often too quick to accept the views of the largest banks.”

A finance ministry spokesperson said the government had examined temporary public ownership of Credit Suisse but it was not “the best available solution.” He said that the government was now reviewing bank regulation.

The spokesperson did not say when they considered nationalization nor elaborate further.

A FINMA spokesperson said the regulator started demanding concrete steps from Credit Suisse as early as the summer of 2022 to prepare for a crisis, showing it recognized the risk of a “destabilization of the bank.” The steps included asking Credit Suisse to prepare for the sale of business units, and later, the sale of the entire bank.

FINMA had alternatives to a sale to UBS, such as a resolution or nationalization of the bank, the spokesperson added.

Spokespeople for the SNB and UBS declined to comment.

The hastily arranged sale to UBS allowed regulators to avoid a messy collapse and wider impact on global financial stability.

Daniel Zuberbuehler, Switzerland’s chief regulator when UBS was bailed out in 2008, said: “It’s difficult to decide when is the right moment to intervene.”

“Had Credit Suisse collapsed, it would have been a nuclear bomb on the economy,” Zuberbuehler said. “Nonetheless, it is no success story that we have lost one of our two big banks.”

Early worries

SNB’s Jordan started worrying about Credit Suisse as early as February 2020, when Tidjane Thiam left as chief executive after it came to light that the bank had spied on some of its top executives, one of the sources with direct knowledge of the matter said.

There was little public display of regulators’ concern, however, as they phrased any warnings about the bank “very carefully” to avoid creating panic, the source said.

Meanwhile, the situation at the bank kept worsening.

In 2020, as the COVID-19 pandemic caused a rush for cash, Credit Suisse struggled to meet its funding needs, according to four people with direct knowledge of the matter.

The crunch, which has not been previously reported, happened as counterparties demanded more collateral for funds, something Credit Suisse had trouble providing. The bank was struggling to cope with large clients drawing down credit lines, two of the sources said.

In its annual report at the time, Credit Suisse said it had seen an increase in net cash outflows in 2020, which weakened its liquidity buffers but the bank maintained it had “strong liquidity and funding.” The details of what happened were not publicly known.

The events led FINMA to force Credit Suisse to hold higher liquidity buffers, three of the sources said. The move would allow the bank to buy more time from regulators in October 2022. Reuters could not determine by how much the buffers were increased.

Credit Suisse’s cash cushions also came under pressure as it was hit by successive scandals, which showed poor risk management practices at the bank. In early 2021, the Swiss lender was hit with losses from dealings with a lender called Greensill amid fraud allegations. Just a few weeks later, it lost billions of dollars when hedge fund Archegos collapsed.

Both episodes led to outflows from the bank, causing Swiss regulators to heighten supervision, with steps such as asking for daily liquidity reports that show how much cash it could easily access, according to a source with direct knowledge of the matter.

Lack of power

FINMA’s powers as a financial regulator are among the weakest in the Western world, lacking some basic tools such as the ability to fine banks, something the agency unsuccessfully lobbied the government from 2021 to change.

That year FINMA went to the Swiss finance ministry, making the case for additional powers as well as the creation of a financial liquidity backstop like the United States and some other jurisdictions have, according to a former Swiss official. A liquidity backstop is a financing facility that banks can tap in an emergency, allowing the central bank to act as the lender of last resort.

In FINMA’s view, the liquidity backstop was crucial as well as a final building block needed for any resolution plan to work, the former official said. In the aftermath of the 2008 financial crisis, global banks such as Credit Suisse were required to create resolution plans, called living wills, which would allow regulators to unwind them without creating broader systemic issues.

At the time, FINMA did not get support from the ministry, the former official said. The finance minister then was Ueli Maurer, a member of the pro-bank Swiss People’s Party.

Under Maurer, the finance ministry had gravitated towards the banks, which were complaining that FINMA was too intrusive, according to three people with direct knowledge of the work of the regulator and banks’ views.

Banks lobbied the government to restrain FINMA’s then-chief executive, Mark Branson, a former banker viewed by the industry as too tough, these people said.

Maurer, who retired in late 2022, did not respond to a request for comment.

In a December 2022 interview with Swiss television, Maurer expressed confidence in Credit Suisse’s ability to turn the corner. “You just have to leave them alone for a year or two,” he said.

In early 2021, Marlene Amstad, a former academic, took over as chair of FINMA. Soon after she started, she began requesting information from FINMA officials about supervision of banks, a move that insiders took as a way for her to look over Branson’s shoulder, one former official said.

Then, she asked to attach additional staff to the supervisory board of FINMA, which would have allowed her to further increase scrutiny of Branson’s team. This executive staff function was eventually not established after FINMA officials resisted, the former official said.

A few months later, Branson left to go to German regulator Bafin. His departure heralded a shake-up that saw the departure of key supervisors responsible for banks and the winding up of troubled lenders.

The FINMA spokesperson said Amstad did not interfere in supervisory work but rearranged the supervisory board’s activity to focus on fewer topics, deepening their understanding of those. The board itself had decided not to pursue the idea of additional staff and the agency’s staffing had not fluctuated much for years, the spokesperson said.

Bank run

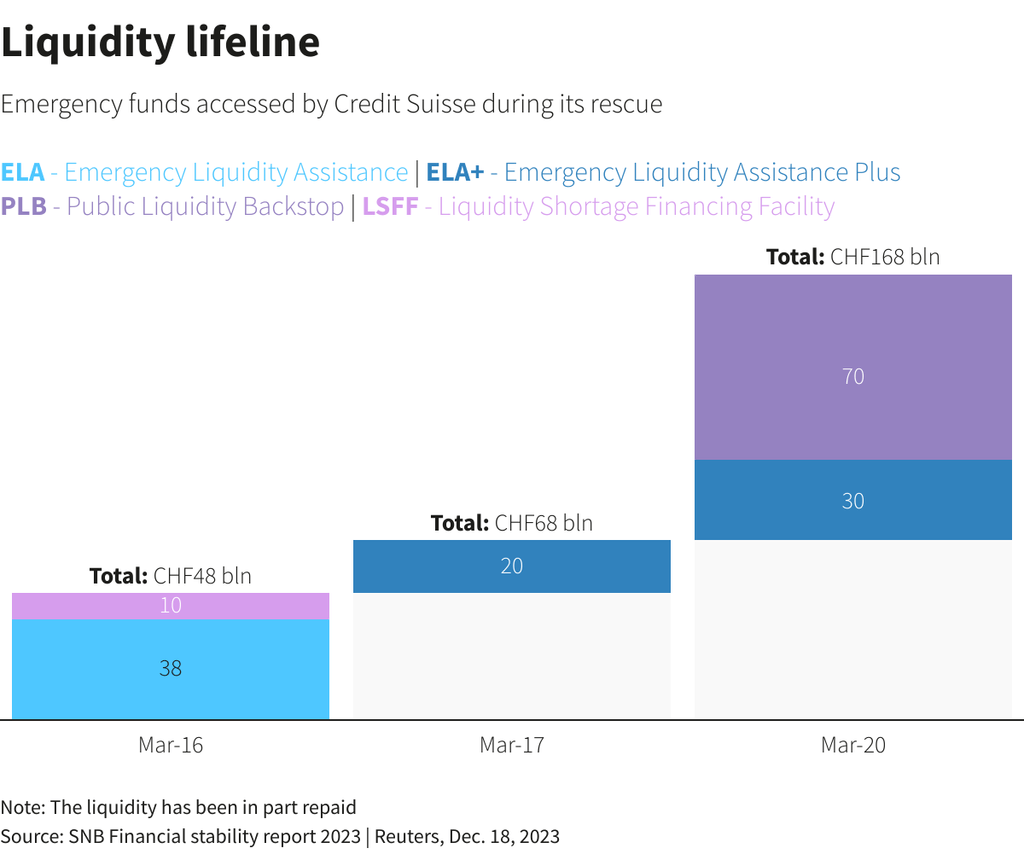

For regulators, the red lights started flashing in October last year, when a social media post from a journalist that a “major international investment bank is on the brink” led to a run on Credit Suisse, two of the sources said.

During the weeks that followed, customers pulled out more than 100 billion francs.

FINMA set up a crisis group, one of the sources said. The regulator also instructed Credit Suisse to prepare contingency plans, including data rooms for a sale of some or all of the business, one source said.

The FINMA spokesperson confirmed the regulator had asked the bank to prepare for a sale.

But FINMA was not in favor of Jordan’s suggestion of nationalizing the bank. One of the sources said FINMA felt replacing the top layer of management would not be effective as its problems went much deeper.

It would be easier for UBS, which could shake up management ranks better than the government could, the source said.

There were also limits to what FINMA could make the bank do. Thanks in part to the buffers put in place during the pandemic, the cash numbers that Credit Suisse reported were within most regulatory requirements, undermining regulators’ ability to force the bank’s hand, three of the sources said.

Still, Credit Suisse said in October 2022 that clients had pulled funds at a pace that saw the lender breach some regulatory requirements for liquidity. Reuters could not learn additional details about the breaches.

Credit Suisse management sought to soldier on without support, a bank executive said. Fearing that news of an emergency funding would leak and trigger disaster, executives warned regulators of the bad “signal” such a move would send, according to one of the sources, who is a former Swiss official.

Despite preparing various press releases to announce a possible central bank facility, illustrating how close it came, the bank ultimately refused, three of the sources said.

Credit Suisse went on to raise $4.2 billion from investors by selling shares later that year. Then withdrawals started to ease, defusing the immediate pressure.

But the calm was brief.

As a regional US banking crisis spread to Europe in March, depositors worried about the safety of their money started withdrawing billions from Credit Suisse once again.

Credit Suisse sought to shore up its finances. Now, it wanted regulators’ help. It calculated that a lifeline of 50 billion francs from the SNB would be enough, according to a Credit Suisse executive with direct knowledge of the matter.

In a scramble for foreign currencies, the SNB turned to the US Federal Reserve, using a little-known line of funding to withdraw about $60 billion, the maximum allowed, without publicity, two sources with knowledge of the matter said.

The Fed declined to comment.

As the SNB dashed to plug funding holes in a desperate bid to keep Credit Suisse afloat, the head of a little-known group of politicians in charge of emergency taxpayer funds, Ursula Schneider Schüttel, received a phone call.

Credit Suisse needed cash – fast.

The new Swiss finance minister, Karin Keller-Sutter, told Schneider Schüttel in a call on the evening of March 16, a Thursday, that they would have to sign off as much money as needed to save Credit Suisse. The country’s financial and economic stability depended on it, she told the Social Democratic politician, according to a source familiar with the matter.

Schneider Schüttel had not been asked for help a few months prior, in October, but now they had to be ready by that weekend.

“It was a blank check,” the source said. “We were told to get ready to approve the funds, but we didn’t know how much.”

That Sunday, UBS agreed to buy Credit Suisse for 3 billion francs in stock, with assistance from the Swiss government.

“After we rescued UBS, the promise was never would this happen again,” Zuberbuehler said. “It has happened again.” – Rappler.com

$1 = 0.8677 Swiss francs

Add a comment

How does this make you feel?

There are no comments yet. Add your comment to start the conversation.