SUMMARY

This is AI generated summarization, which may have errors. For context, always refer to the full article.

![[ANALYSIS] Will corporate tax cuts help the economy recover from the COVID-19 pandemic?](https://www.rappler.com/tachyon/2020/08/tl-tax-cut-corporate.jpg)

The COVID-19 pandemic, initially downplayed by the government, continues to be a public health emergency. As the country struggles with its containment, it has also become an urgent socio-economic issue.

According to the Philippine Statistics Authority (PSA), the economy, as measured by GDP, contracted by 0.7% in the first quarter of 2020 and 16.5% in the next quarter, the deepest recession in more than 30 years. This coincided with an unemployment rate of 17.7% in April 2020, the highest so far since 2005. The crisis is also predicted to cause an increase in the number of the poor, effectively reversing significant poverty reduction in the past 10 years.

To bounce back, the economy needs stimulus. Expansionary fiscal policy is one approach to stimulate economic activities. This is usually done by increasing government spending through public works, transfers, and subsidies. Tax cuts are also considered an expansionary fiscal policy as liquidity is retained in the private sector for investment activities.

The government is currently pushing corporate tax cuts through the Corporate Recovery and Tax Incentives for Enterprises Act (CREATE) bill. This bill proposes a reduction of 5 points for 2020-2022 and an additional 1-point in each of the succeeding years until 2027. Corporate tax cuts are just one among the provisions of CREATE that seeks to rationalize the government’s fiscal incentive system.

According to the government, this sharp reduction in corporate tax rates starting in 2020 must be considered part of the government’s economic recovery program. It is assumed that lower tax rates free up additional financial space for firms which they, supposedly, will use for operation or even expansion of their economic activities.

Does this assumption still hold true in the context of the COVID-19 pandemic when demand in the market has been seriously impaired because of the economic crisis? Do firms still have the incentive to expand when faced with weak demand because of lower incomes due to the crisis?

A simulation exercise

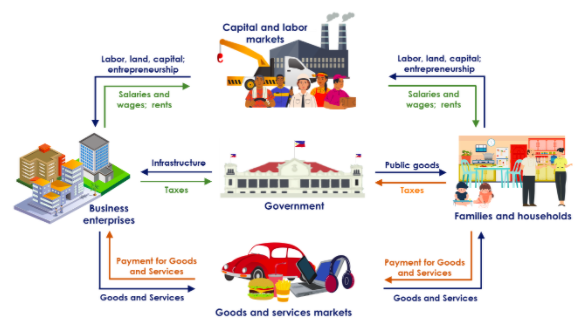

To answer this question, we did some experiments using a computable general equilibrium model (CGE). A CGE is a quantitative analytical tool that represents the modelers’ view of how the economy works: households consume using income they earn from work or investments, and firms earn profits by selling goods produced using labor and capital. This system is best summarized by the familiar circular diagram below.

In the real world, governments intervene in the economy through taxation (or subsidies), provision of public goods, and regulation. Most CGE models in policy applications, therefore, also include the government.

A CGE is calibrated using actual data to provide the baseline scenario. Hence, simulations done using CGE models can be thought of as an experiment carried out in a parallel world. In this exercise, we used data on the Philippine economy in 2015. In the model, households, firms, government, and the rest of the world transact with each other. Just as in any economic model, the assumptions of the model are also its limitations. Although simulation results are not projections about the impact of economic shocks, they remain useful in ex ante evaluations of economic policies because they provide insights about the possible response of the economy to these shocks and policies through the counterfactual scenarios.

Simulation results

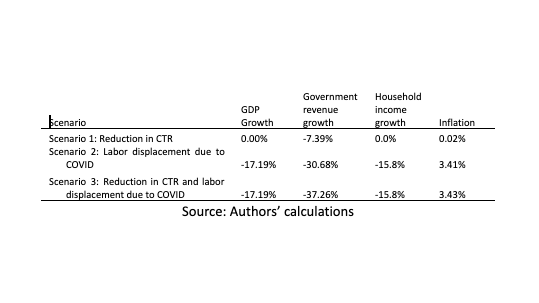

There were 3 simulation scenarios. First, we reduced corporate income taxes (CTR) equivalent to the proposed 5-point reduction in the CREATE bill to capture the impacts of the tax cuts alone. Second, we attempted to recreate labor displacement caused by the COVID-19 lockdown. Previously, it was estimated that 57% of the employed were displaced, which is equivalent to about 40% reduction in potential employment income. Third, we incorporated both shocks in Scenarios 1 and 2 to capture how the proposed tax cut interacts with the economic impacts of the lockdown. The results of the simulation are shown in Table 1.

Scenario 1 shows that the reduction in CTR has no discernible impact on GDP growth, household incomes, and only minimal impact on prices. However, and as expected, it will reduce government revenues.

On the other hand, Scenario 2 shows that the labor displacement caused decline in GDP by 17%. Economic contraction also reduces both government revenues and household incomes.

If corporate tax cuts are meant to stimulate the economy as a response to the recession brought by the pandemic, then we should expect to observe significant growth in GDP in Scenario 1 and an improvement in GDP growth in Scenario 3. However, this is not supported by the simulation results. Meanwhile, tax cuts are shown to reduce government revenues.

Decreased tax revenues further threatens our capacity to support economic recovery and would potentially require other means of raising funds (such as printing money or borrowing) in the long run.

Future work

Our simulation attempted to replicate the economic impacts of the pandemic, as well as provide an alternative view about the economic impact of corporate tax cuts. In the future, we will expand this simulation exercise to examine the soundness of other components of various proposed stimulus programs: wage subsidies, transfers to households, and government infrastructure spending. – Rappler.com

CJ Castillo is a program coordinator and an economist at Labor Education and Research Network (LEARN).

Marjorie Muyrong is an economist at the Ateneo Center for Economic Research and Development (ACERD) and a PhD Sociology candidate at La Trobe University, Australia.

The opinions expressed in this article are those of the authors. The model and the data used in this article are available here. The model runs in General Algebraic Modeling System (GAMS).

Add a comment

How does this make you feel?

![[Time Trowel] Evolution and the sneakiness of COVID](https://www.rappler.com/tachyon/2024/02/tl-evolution-covid.jpg?resize=257%2C257&crop=455px%2C0px%2C1080px%2C1080px)

There are no comments yet. Add your comment to start the conversation.